Overview

The recent intensification of the coronavirus (COVID-19) pandemic has weakened the near-term outlook for euro area activity but not derailed the recovery. Despite extended and more stringent containment measures, activity in the fourth quarter of 2020 declined by significantly less than expected in the December 2020 Eurosystem staff projections due to learning effects, strong manufacturing growth and a rebound in foreign demand. Although the new lockdowns have been accompanied by additional fiscal support measures, another decline in activity is projected for the first quarter of 2021. The near-term outlook for activity depends on the evolution of the pandemic and, in particular, on how fast and how much rising vaccination rates will allow an unwinding of containment measures. Containment measures are now assumed to be more stringent in the first half of 2021 than in the December 2020 projections, before concerted efforts to ramp up the production and distribution of vaccines allow a stronger relaxation of containment measures and a final resolution of the health crisis by early 2022, in line with the previous projections. This, together with substantial support from monetary and fiscal policy measures – including, in part, Next Generation EU (NGEU) funds – and a further recovery in foreign demand, should lead to a firm rebound as of the second half of 2021, with real GDP expected to exceed its pre-crisis level from the second quarter of 2022, one quarter earlier than previously projected. Thus, the medium-term outlook for real GDP is expected to be broadly similar to that foreseen in the December 2020 projections. As policy measures are expected to be successful in averting large financial amplification effects and limiting the economic scars of the crisis, real GDP is expected to stand 3.3% above its 2019 pre-crisis level by the end of 2023.[1]

Inflation will be subject to considerable volatility over the coming quarters, but over the medium term underlying price pressures are expected to remain subdued due to weak demand and to strengthen only gradually in line with the economic recovery. The combined upward impact from the recent surge in oil prices, the end of the temporary VAT rate reduction in Germany and upward data surprises imply a temporary jump in HICP inflation in 2021, which has been revised up by 0.5 percentage points compared with the December 2020 projections. While most of the large upward surprise in HICP inflation excluding energy and food observed in January 2021 is assessed to relate to temporary effects, including statistical factors such as changes in HICP weights and price imputations, a small part is likely to have a more persistent impact. Overall, HICP inflation is expected to rebound sharply from 0.3% in 2020 to 1.5% in 2021, peaking at 2.0% in the last quarter of 2021, before dropping to 1.2% in 2022 and then increasing to 1.4% in 2023. Compared with the December 2020 Eurosystem staff projections, HICP inflation has been revised up notably for 2021, related mainly to much higher oil prices, and slightly for 2022, but is unchanged for 2023.

The international environment of the March 2021 ECB staff projections does not take account of the recently approved fiscal package in the United States, due to the uncertainty with respect to its size, composition and timing at the time of the cut-off date. The related risks to the projections for the US and euro area economies are presented in Box 4.

In view of the continued significant uncertainty regarding the evolution of the pandemic and the degree of economic scarring, two alternative scenarios have again been prepared. The mild scenario envisages a more successful roll-out of the vaccines, allowing for a phasing out of containment measures by the end of 2021, while faster learning effects limit the economic costs. In this scenario, real GDP would rebound by 6.4% in 2021, reaching its pre-crisis level in the third quarter of the year, with inflation rising to 1.7% in 2023. In contrast, the severe scenario envisages a strong intensification of the pandemic, with new variants of the virus also implying a reduction in the effectiveness of vaccines, leading governments to maintain some containment measures until mid-2023 with substantial and permanent losses to economic potential. Under this scenario, real GDP would grow by just 2.0% in 2021 and would not reach its pre-crisis level within the projection horizon, with inflation at only 1.1% in 2023. These alternative scenarios are presented in Section 5.

1 Key assumptions underlying the projections

The baseline rests on the assumptions of a swift relaxation of containment measures from the second quarter of this year and a resolution of the health crisis in early 2022. Containment measures in the euro area became more stringent in early 2021 and are assumed to be relaxed only towards the end of the first quarter. On average, they are expected to be more restrictive than in the fourth quarter of 2020 and what was assumed in the December 2020 projections. From the second quarter of 2021, the baseline assumes a swift relaxation of containment measures, mainly on account of concerted efforts to speed up vaccination through the approval of additional vaccines and new vaccine production facilities. Overall, containment measures are expected to have been completely withdrawn by early 2022, unchanged from the previous projections. Similar assumptions regarding the evolution of the pandemic are, on average, made for the international environment.

Significant monetary and fiscal policy measures, including the NGEU package, will help support incomes, reduce job losses and bankruptcies, and be successful in containing adverse real-financial feedback loops. In addition to the monetary policy measures taken by the ECB up to the cut-off date for the projections, the baseline includes discretionary fiscal policy measures related to the COVID-19 crisis amounting to about 4¼% of GDP in 2020 and 3¼% of GDP in 2021 (Section 3). Government loans and guarantees or capital injections should contribute to alleviating liquidity constraints. Furthermore, supervisory and macroprudential policies have freed up bank capital to absorb losses and to support the flow of credit to the real economy through the release of capital buffers, guidance to reduce procyclical provisioning and measures to preserve banks’ loss-absorbing capacity. Importantly, the monetary, fiscal and prudential policy measures are assumed to be broadly successful in avoiding severe real-financial feedback loops over the projection horizon.

Box 1

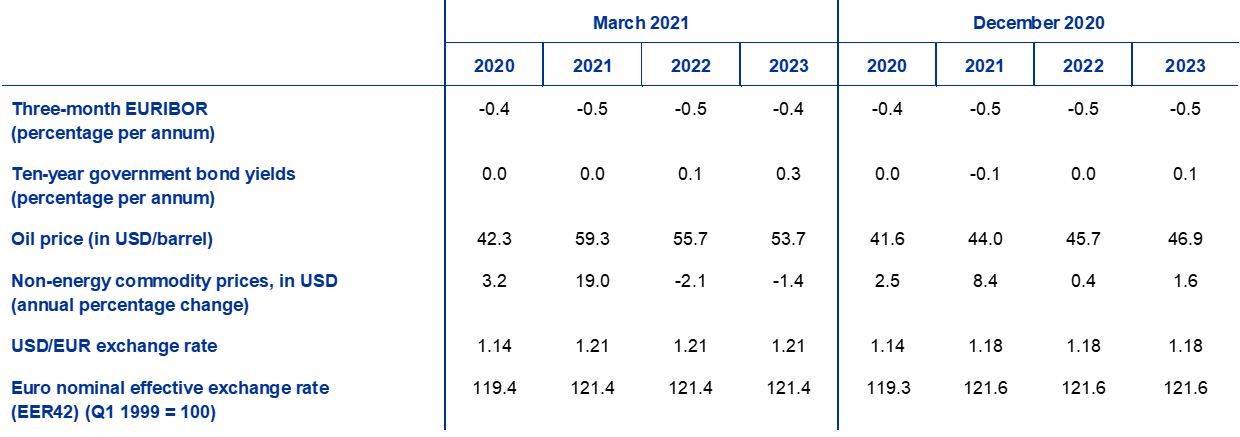

Technical assumptions about interest rates, commodity prices and exchange rates

Compared with the December 2020 projections, the current technical assumptions include higher long-term interest rates, significantly higher oil prices and a slightly weaker effective exchange rate of the euro. The technical assumptions about interest rates and commodity prices are based on market expectations with a cut-off date of 16 February 2021. Short-term interest rates refer to the three-month EURIBOR, with market expectations derived from futures rates. The methodology gives an average level for these short-term interest rates of -0.5% in 2021 and 2022, and of -0.4% in 2023. The market expectations for euro area ten-year nominal government bond yields imply an average annual level of 0.0% for 2021, 0.1% for 2022 and 0.3% for 2023.[2] Compared with the December 2020 projections, market expectations for short-term interest rates have marginally increased for 2023, while market expectations for euro area ten-year nominal government bond yields have increased by 10 to 20 basis points for 2021-23.

As regards commodity prices, the projections consider the path implied by futures markets by taking the average for the two-week period ending on the cut-off date of 16 February 2021. On this basis, the price of a barrel of Brent crude oil is assumed to rise from USD 42.3 in 2020 to USD 59.3 in 2021, before declining to USD 53.7 by 2023. This path implies that, in comparison with the December 2020 projections, oil prices in US dollars are around 35% higher in 2021 and 14% higher in 2023, while the oil price futures curve has become downward sloping in contrast to the upward sloping curve underlying the previous projections. The prices of non-energy commodities in US dollars are assumed to rebound strongly in 2021, but to decrease moderately over the remainder of the projection horizon.

Bilateral exchange rates are assumed to remain unchanged over the projection horizon at the average levels prevailing in the two-week period ending on the cut-off date of 16 February 2021. This implies an average exchange rate of USD 1.21 per euro over the period 2021-23, which is 2% higher than the assumptions entailed in the December 2020 projections. The assumption for the effective exchange rate of the euro has been revised down by 0.2% since the December 2020 projection exercise.

Technical assumptions

2 Real economy

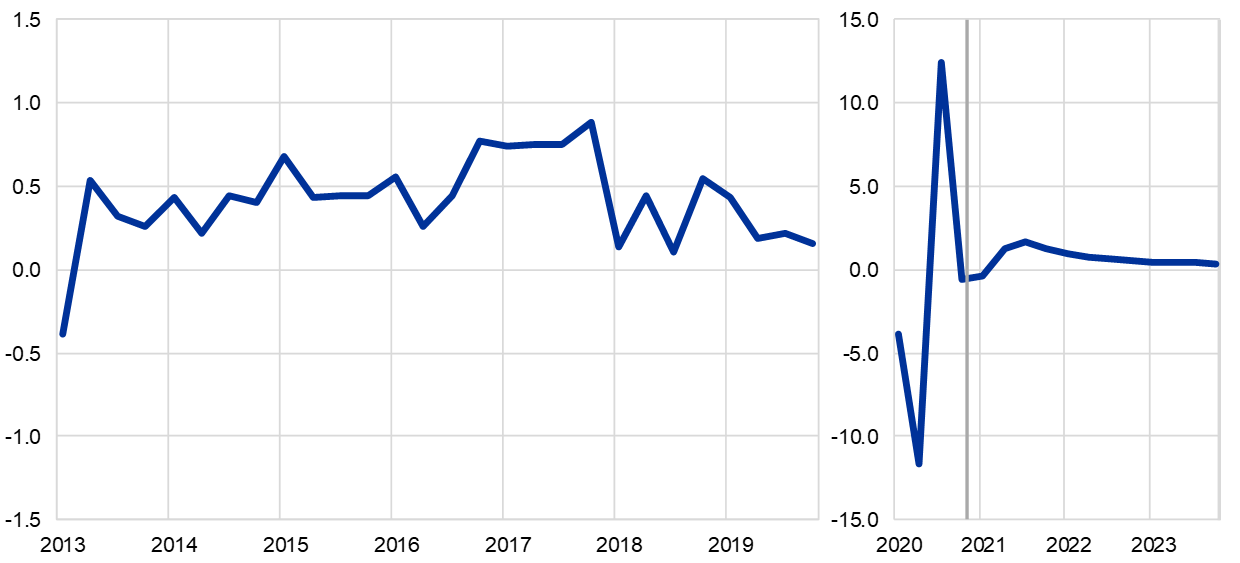

Real GDP declined in the fourth quarter of 2020 but by much less than expected. Real GDP declined by 0.7% in the fourth quarter, substantially less than the -2.2% expected in the December 2020 baseline and even less than envisaged in the mild scenario. This upward surprise, despite containment measures being more stringent than expected, may partly relate to stronger than expected foreign demand but also seems to reflect learning effects as agents better adjust to containment measures across all economic sectors. Overall, the level of real GDP in the fourth quarter of 2020 was 4.9% below its level in the fourth quarter of 2019.

Chart 1

Euro area real GDP

(quarter-on-quarter percentage changes, seasonally and working day-adjusted quarterly data)

Notes: In view of the unprecedented volatility in real GDP in the course of 2020, the chart shows a different scale from early 2020. The vertical line indicates the start of the projection horizon. This chart does not show ranges around the projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Section 5.

Containment measures in early 2021 are expected to lead to a further slight contraction in real GDP in the first quarter, followed by a modest increase in the second quarter. Faced with higher numbers of new COVID-19 cases and the threat of another wave caused by mutations of the virus, many euro area countries extended and further tightened lockdown measures in early 2021. Short-term forecasting models based on the available data at the cut-off date, such as the composite output Purchasing Managers’ Index (which stood at 48.1 in February) and other high-frequency indicators, also suggest a muted decline in real GDP in the first quarter. As in the fourth quarter of 2020, containment measures are expected to result in less of a disturbance to manufacturing activities but to weigh further on activity in the services sector. Recently announced targeted fiscal measures to support the sectors affected by the lockdown are also likely to mitigate the overall loss in activity. Overall, real GDP is expected to decline by 0.4% in the first quarter of 2021 (compared with an increase of 0.6% in the December 2020 projections) and to increase by 1.3% in the second quarter (compared with 1.7% in the previous projections).

Activity is projected to rebound strongly during the second half of 2021, as containment measures are expected to be relaxed. The expected rebound is based on the assumption of a swift relaxation of containment measures, a further decline in uncertainty, a boost to confidence in the wake of an expected acceleration in vaccination, a continued robust recovery in foreign demand, supportive fiscal and monetary policies and some pent-up demand. It will be mainly driven by domestic demand, in particular private consumption. Real GDP is expected to exceed its pre-crisis level of the fourth quarter of 2019 in the second quarter of 2022 and to stand 3.3% above its pre-crisis level in the last quarter of the projection horizon.

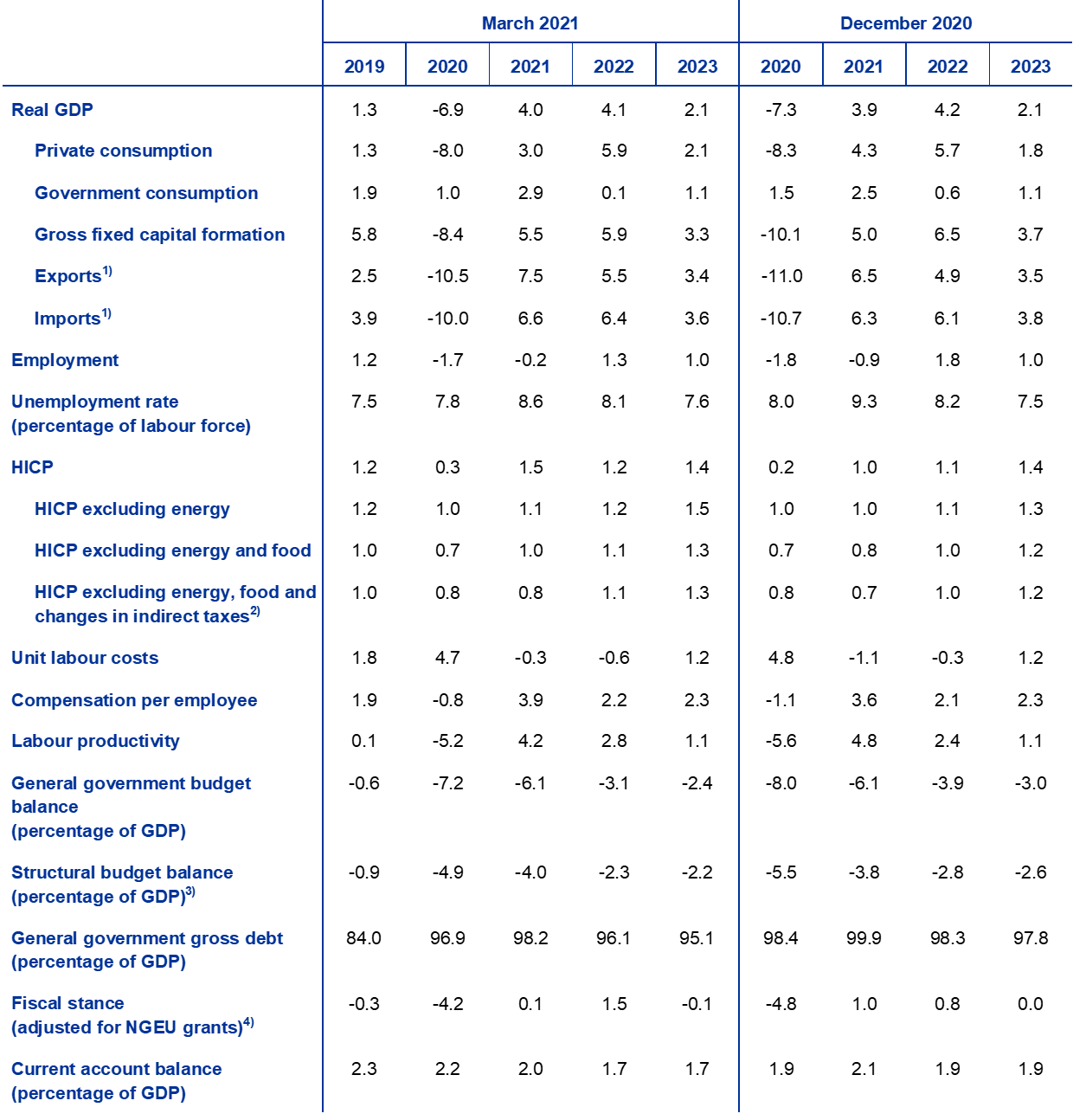

Table 1

Macroeconomic projections for the euro area

(annual percentage changes)

Notes: Real GDP and components, unit labour costs, compensation per employee and labour productivity refer to seasonally and working day-adjusted data. The figures may differ from the latest Eurostat publications due to data releases after the cut-off date for the projections. This table does not show ranges around the projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Section 5.

1) This includes intra-euro area trade.

2) The sub-index is based on estimates of actual impacts of indirect taxes. This may differ from Eurostat data, which assume a full and immediate pass-through of indirect tax impacts to the HICP.

3) Calculated as the government balance net of transitory effects of the economic cycle and measures classified under the European System of Central Banks (ESCB) definition as temporary.

4) The fiscal policy stance is measured as the change in the cyclically adjusted primary balance net of government support to the financial sector. The figures shown are also adjusted for expected NGEU grants on the revenue side.

Private consumption is expected to recover strongly in 2021 and to remain the key driver of the recovery thereafter. Following the robust but incomplete rebound in the third quarter of 2020, private consumption decreased again in the fourth quarter of 2020, reflecting further lockdowns and increased containment measures, and was the main driver of the renewed downturn in economic activity. However, the renewed decline in consumption was smaller than previously expected, possibly reflecting the use of more targeted containment measures and learning effects among private households (such as increased recourse to online shopping). The strong fluctuations and overall decline in the level of private consumption in the course of 2020 contrast with more contained developments in real disposable income, stabilised by government support, leading to significant changes in the saving ratio. Looking ahead, private consumption is expected to decline further in the first quarter of 2021 as a consequence of the further tightening of containment measures, resulting in another small increase in the saving ratio. Private consumption is projected to resume its recovery from the second quarter of 2021 and to exceed its pre-crisis level in the third quarter of 2022. This rebound should be supported by gradually declining uncertainty and a gradual convergence of the saving ratio to its pre-crisis level, as both forced and precautionary savings are expected to unwind, while elevated unemployment and an unwinding of net fiscal transfers will likely act as a drag on the recovery.

The sharp and sudden contraction in housing investment in 2020 is expected to be reversed gradually over the projection horizon. Housing investment increased by 0.5% in the fourth quarter of 2020 but was still almost 3% below its pre-pandemic level. Looking ahead, with expected house price inflation outperforming housing costs, positive Tobin’s Q effects and a rebound in disposable income should support housing investment. However, weak consumer confidence and higher unemployment, compared with its pre-crisis level, for most of the projection horizon are likely to dampen, in the medium term, the recovery in housing investment, which is expected to return to its pre-crisis level by the end of 2022.

Business investment is expected to recover substantially in 2021 and 2022, reaching its pre-crisis level in early 2022. It is estimated to have rebounded significantly in the second half of 2020, partially recovering from its weakness in the first half of the year. Following another mild contraction in the first quarter of 2021 in the context of weak overall activity, a further rebound is expected to start from the second quarter of 2021, as global and domestic demand recover and profit growth turns positive again, and also supported by assumed favourable financing conditions and the positive impact of the NGEU plan on business investment.

The gross indebtedness of non-financial corporations, which increased significantly in 2020, is expected to decline moderately while remaining above its pre-crisis level at the end of the projection horizon. The increase in gross indebtedness was due to a sharp fall in corporate profits in the first lockdown phase and the resulting increased recourse to debt financing to compensate for liquidity shortfalls. Looking ahead, following a further slight increase in the near term, corporate gross indebtedness is expected to decline moderately to stand in 2023 significantly above its already elevated pre-crisis level. The increase in the gross debt ratio is expected to limit business investment growth over the projection horizon, notwithstanding strong cash holdings, as firms have to restore their balance sheet health. At the same time, possible debt sustainability concerns should be eased by corporate gross interest payments, which are expected to increase only modestly in the coming years from record low levels.

Box 2

The international environment

In the second half of 2020 the global economy rebounded from the pandemic-induced recession faster than previously expected. Global investment – benefiting from favourable financing conditions amid strong monetary policy support – is already close to pre-pandemic levels, while the recovery in global consumption, supported by fiscal measures to bolster income and preserve jobs, continues to lag, as prevailing containment measures weigh on contact-intensive services. Global (excluding the euro area) real GDP growth rebounded strongly, by 7.4%, in the third quarter of 2020, 0.7 percentage points more than expected in the December 2020 projections. A more dynamic pace of recovery was observed in both advanced and emerging market economies. Following this V-shaped rebound, the recovery in global economic activity is expected to continue in the fourth quarter of 2020 at a robust but more moderate pace of 2.1%, still stronger than in the previous projections.

Headwinds to the recovery intensified as the global pandemic worsened at the turn of the year. An increase in new infections led governments to reimpose more stringent lockdowns, particularly in advanced economies. In contrast, containment measures in emerging market economies were tightened less. However, overall, the renewed lockdowns imply a setback to global growth in the first quarter of 2021, as evidenced by high-frequency trackers of economic activity in key advanced economies. While global (excluding the euro area) composite and manufacturing PMIs stood above their long-term average in February, some of their components signalled weaker activity ahead. For instance, new export orders declined below the expansionary threshold in January for the first time since September 2020 and stayed below it in February.

Nevertheless, the EU-UK trade deal and the December 2020 USD 0.9 trillion US fiscal stimulus package imply a stronger outlook for global growth in 2021, while the additional fiscal stimulus, recently approved by the US Congress, represents an upside risk for the US and global economies. The EU-UK trade deal replaces the no-deal Brexit assumption underpinning the December 2020 projections. It ensures tariff-free goods trade and zero quotas between the European Union and the United Kingdom (like the CETA agreement with Canada), thereby boosting activity and trade in the UK economy over the projection horizon. In the United States, the fiscal stimulus agreed in December 2020 amounts to USD 0.9 trillion (4.4% of GDP) and is projected to raise real GDP growth by more than 1 percentage point in 2021. The recently approved additional fiscal package totalling USD 1.84 trillion has not been taken into account in the baseline and is therefore an important upside risk to the current projection baseline (Box 4).

Overall, global GDP (excluding the euro area) is projected to increase by 6.5% in 2021, before decelerating to 3.9% and 3.7% in 2022 and 2023 respectively. This follows the estimated 2.4% contraction in global real GDP growth in 2020. Growth has been revised up by 0.7 percentage points in 2021, as the positive impact of a carry-over from the surprises towards the end of last year and more supportive economic policies are only partly offset by the negative impact on growth of tighter containment measures in the near term.

Given the depth of last year’s global recession, global trade in goods has remained relatively resilient, while trade in services continues to be depressed. This relates mainly to the fact that the overall economic contraction has been tilted more towards the less trade-intensive services sector, and substitution between services and goods consumption in advanced economies has likely lent support to goods trade during the pandemic crisis. This is supported by incoming data, which suggest that global goods imports returned to their pre-pandemic level in November 2020. While the recovery in global trade in goods was swift, tight transport capacities and rising shipping costs weighed on trade, and supply shortages – particularly in Asian IT sectors – signal risks for global supply chains. Such factors are evidenced by a steady lengthening of supplier delivery times and are likely to weigh on trade in goods in the near term. At the same time, international travel services, which account for around 7% of global trade in goods and services, remain constrained as a result of the pandemic and associated travel restrictions.

Global (excluding the euro area) import growth has been revised up considerably for 2021. Imports are expected to increase by 9.0% in 2021, before decelerating to 4.1% and 3.4% in 2022 and 2023 respectively. Compared with the December 2020 projections, global imports and particularly euro area foreign demand have been revised up significantly owing to the EU-UK trade deal and, to a lesser extent, a projected stronger recovery in advanced economies. This implies that euro area foreign demand is projected to increase by 8.3% this year and by 4.4% and 3.2% in 2022 and 2023 respectively, resulting in a notable upward revision for 2021 and a smaller revision for 2022.

The international environment

(annual percentage changes)

1) Calculated as a weighted average of imports.

2) Calculated as a weighted average of imports of euro area trading partners.

The recovery in foreign demand is expected to sustain export growth, leading to a positive net trade contribution in 2021 that will turn neutral thereafter. The support from strong foreign demand sustained the recovery in euro area exports, which registered robust growth in the fourth quarter of 2020 despite the reintroduction of restrictions. While a shift in demand from services to consumer goods boosted euro area manufacturing exports, the recovery in services exports – particularly travel services – remained subdued. As of 2021, the solid foreign demand should buffer export growth, while COVID-related uncertainty, bottlenecks in the logistics sectors and losses in export price competitiveness owing to the past appreciation of the euro may have a dampening effect. As pandemic dynamics weigh on internal demand conditions, imports are expected to grow less than exports in 2021, hence the net trade contribution to GDP will turn positive in 2021 but will be broadly neutral in 2022 and 2023.

Following repeated positive surprises, the labour market outlook is stronger than projected in the December 2020 projections, with only small increases in the unemployment rate expected in the coming quarters. The unemployment rate increased from 7.4% in the second quarter of 2020 to 8.2% in the fourth quarter, yet another surprise relative to the figure of 8.8% expected in the December projections following overpredictions in the previous two staff projection exercises. The surprise was once again due to much more resilient employment and an unexpected increase in the number of workers in job retention schemes, following the second wave of lockdown measures. Employment in the fourth quarter of 2020 was, nevertheless, still 1.9% below the level in the fourth quarter of 2019. As the labour market starts to normalise and workers exit job retention schemes, the unemployment rate is projected to rise further to peak at 8.7% in the second quarter of 2021 (revised down from 9.5% in the December 2020 projections), before declining to 7.5% by the end of 2023 as the economy recovers. This projection assumes that a high share of workers in job retention schemes can return to regular employment. By the end of the projection horizon, the unemployment rate and the number of persons employed are expected to converge towards, but not reach, pre-crisis levels.

Labour productivity growth per person employed is projected to recover from the start of 2021. Following the recovery from the sharp drop in the first half of 2020, labour productivity per person declined again in the fourth quarter of the year, owing to intensified containment measures and the related increase in the use of job retention schemes in many countries. The growth of labour productivity per person is projected to recover in the first half of 2021 before gradually moderating over the remainder of the projection horizon. The growth profile of productivity per hour worked has been much more muted during the pandemic, as total hours worked are expected to closely follow developments in GDP. By the end of the projection horizon, productivity per hour worked is expected to grow gradually to stand about 3% above its pre-crisis level.

Compared with the December 2020 projections, the profile for annual real GDP growth is broadly unchanged, reflecting several offsetting factors. The broadly unchanged projection for real GDP growth for 2021 reflects the weaker short-term outlook, primarily due to the lockdown extensions, which offsets the upward surprise in the fourth quarter of 2020 and some upward revisions for the second half of 2021. These upward revisions are on account of a stronger expected rebound, as the more stringent of containment measures in the first half of the year are assumed to be relaxed at a faster pace than assumed in the December projections. In addition, growth is supported by the upward impact of stronger foreign demand and additional fiscal stimulus. In 2022 some positive carry-over from the stronger rebound in the second half of 2021 is expected to offset a negative impact from the assumptions, notably higher oil prices and the withdrawal of the additional fiscal support in 2021.

3 Fiscal outlook

After the strong fiscal expansion in 2020, continued fiscal support is expected to mitigate the macroeconomic impact of the COVID-19 crisis in 2021 and further underpin the recovery. In 2020, the fiscal stimulus measures taken by governments in response to the pandemic are assessed to amount to about 4¼% of GDP, slightly below the assumptions of the December 2020 projections. As regards 2021, governments have prolonged emergency measures in the light of the new round of lockdown restrictions, expanded their size and/or adopted new support measures, estimated to total 3¼% of GDP. Most of the additional measures are temporary and are expected to be reversed in 2022. Some have been extended further, and together with other recovery measures, including the NGEU-funded spending[3], entail an annual stimulus of about 1½% of GDP over 2022-23. In terms of composition, as in 2020, most of the 2021 support is additional spending in the form of subsidies and transfers to firms, including under job retention schemes, and increased government consumption. On the revenue side, measures mostly refer to further cuts in direct and indirect taxes. Additional government investment, while limited in 2020, has a higher share as of 2021, mainly on the back of expected NGEU-grant financing. Adjusting for the impact of NGEU grants, the fiscal stance[4] is projected to be broadly neutral in 2021, with the previously expected tightening now postponed to 2022.

After the substantial decline in 2020 to -7.2% of GDP, the euro area budget balance is projected to recover somewhat in 2021 and to stand at -2.4% of GDP in 2023. The improvement in the budget balance in 2021 reflects the decline in the cyclically adjusted primary deficit, as part of the additional spending is expected to be funded by NGEU grant revenue, as well as a somewhat better cyclical component and lower interest payments. The more sizeable improvement in the budget balance in 2022 is mainly due to the unwinding of most of the emergency stimulus measures and a more favourable cyclical component. Finally, in 2023, with a broadly neutral fiscal stance and better cyclical conditions, the aggregate budget balance is projected to improve further to -2.4% of GDP. Interest payments are projected to decline further over the projection horizon and to amount to 1.1% of GDP in 2023. Compared with the December 2020 projections, the euro area budget balance path has been revised up, apart from 2021, when the temporary additional stimulus offsets the improved cyclical conditions and the base effect of a less expansionary fiscal stance in 2020.

Euro area debt is projected to peak in 2021 at 98% of GDP, declining slightly thereafter. The decline over 2022-23 is due mainly to favourable interest-growth differentials, which more than offset the continuing, albeit decreasing, primary deficits.

4 Prices and costs

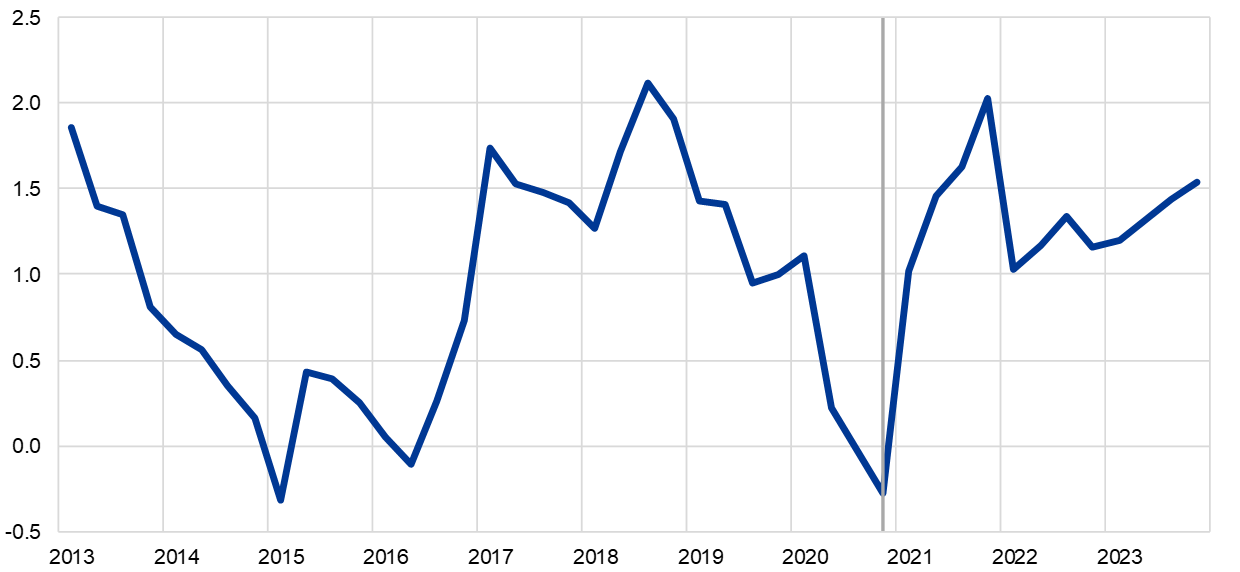

HICP inflation is expected to rise sharply from 0.3% in 2020 to an average of 1.5% in 2021, peaking at 2.0% in the fourth quarter of the year, and to fall back to 1.2% in 2022 before rising to 1.4% in 2023 (Chart 2). HICP inflation increased significantly in January 2021 to 0.9%, from -0.3% in December 2020. This increase was mainly driven by a sharp increase in HICP inflation excluding energy and food, which was partly due to a sizable change in HICP weights, reflecting changed consumption behaviours in the context of the pandemic in 2020.[5] Besides the impact of weight changes, the jump in headline inflation also reflected a number of temporary factors: the end of the temporary VAT reduction in Germany, delays in sales periods in some countries and the impact of the recent surge in oil prices on HICP energy inflation. In addition, a sizeable share of imputed prices for HICP inflation excluding food and energy in January 2021 (18%) implies higher than usual uncertainty as regards actual price pressures in the economy. Looking ahead, HICP inflation is expected to rise to 2.0% in the fourth quarter of 2021. As the impact of temporary factors drop out of the annual rates, inflation is expected to fall back to 1.0% at the beginning of 2022, before increasing gradually to 1.4% in 2023.[6] Following a strong swing from -6.8% in 2020 to 6.1% in 2021, HICP energy inflation is expected to have a broadly neutral contribution to headline HICP inflation in 2022 and 2023. HICP food inflation in 2021 is expected to reverse its COVID-related surge of 2020, but to increase again from mid-2022 to stand at 1.9% in 2023.

HICP inflation excluding energy and food is expected to increase from 0.7% in 2020 to 1.3% in 2023, displaying strong quarterly volatility in 2021 and 2022. This volatility relates especially to changes in HICP weights and impacts from indirect taxes, which are expected to lead to a trough in HICP inflation excluding energy and food in the summer, followed by a rather strong pick-up in the last quarter of 2021. Abstracting from the impacts of weight changes and changes in indirect taxes, underlying inflation is expected to gradually strengthen in the context of the ongoing economic recovery.

Chart 2

Euro area HICP

(annual percentage changes)

Notes: The vertical line indicates the start of the projection horizon. This chart does not show ranges around the projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, in order to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Section 5.

Job retention schemes imply strong volatility in compensation per employee growth, but they cushion the impact of movements in economic activity on firms’ wage costs. These schemes mainly affect compensation per employee in 2021. The schemes safeguard employment in the presence of a significant reduction in hours worked, pushing down the annual growth rate of compensation per employee. As the impact of these schemes gradually fades and labour market developments normalise, growth in compensation per employee is expected to increase gradually to 2.3% in 2023, slightly above the rates seen prior to the pandemic.

Beyond strong fluctuations in 2021, growth in unit labour costs is expected to provide, on balance, only muted inflationary pressures. The strong fluctuations largely reflect expected developments in productivity rather than in wages. Strong labour productivity growth in 2021, when production recovers but labour markets remain sluggish, and, to a lesser extent, in 2022, is expected to lead to negative unit labour cost growth in these two years before it returns to modest positive territory in 2023.

Import price dynamics are expected to be strongly influenced by oil price movements and reflect moderate external price pressures over the latter part of the projection horizon. The annual growth rate of the import deflator is expected to move from -1.6% in 2020 to 3.3% in 2021, largely reflecting increases in oil prices, before slowing to more moderate rates of around 1%. In addition to higher oil prices, the positive import price inflation rate as of 2021 also reflects some upward price pressures from non-energy commodity prices, as well as positive impacts from a reduction in global slack as the world economy recovers.

Compared with the December 2020 projections, the outlook for HICP inflation has been revised up for 2021 and 2022 but is unchanged for 2023. HICP energy inflation has been revised up for 2021 and revised down for 2022 and 2023, reflecting the assumption embedded in the oil price futures curve. HICP food inflation has been revised down for 2021, reflecting weaker data outturns, but revised up for 2022 and 2023 in line with stronger food commodity price assumptions. HICP inflation excluding energy and food has been revised marginally up over the projection horizon on account of recent data surprises, which are largely but not fully assessed to be due to temporary factors, and somewhat higher private sector inflation expectations.

Box 3

Forecasts by other institutions

A number of forecasts for the euro area are available from both international organisations and private sector institutions. However, these forecasts are not strictly comparable with one another or with the ECB staff macroeconomic projections, as they were finalised at different points in time. They were also likely based on different assumptions about the future evolution of the COVID-19 pandemic. Additionally, these projections use different methods to derive assumptions for fiscal, financial and external variables, including oil and other commodity prices. Finally, there are differences in working day adjustment methods across different forecasts (see the table).

The March 2021 projections are broadly comparable with other forecasts for growth, while inflation is above other forecasts for 2021 and broadly in line thereafter. The March projections for growth are within the range of other forecasts in 2021 but at the upper end in 2022-23. As regards inflation, the March 2021 projection for 2021 is notably higher, which is likely due to the inclusion of the most recent increases in oil prices and the January 2021 outcome. For the remainder of the projection horizon, the March 2021 projection is broadly in line with other forecasters.

Comparison of recent forecasts for euro area real GDP growth and HICP inflation

(annual percentage changes)

Sources: MJEconomics for the Euro Zone Barometer, 18 February 2021, data for 2023 are taken from the January 2021 survey; Consensus Economics Forecasts, 11 February 2021, data for 2023 are taken from the January 2021 survey; European Commission Winter 2021 Interim Economic Forecast; ECB Survey of Professional Forecasters, for the first quarter of 2021, conducted between 7 and 11 January 2021; OECD March 2021 Economic Outlook Interim Report for real GDP growth, OECD December 2020 Economic Outlook No 108 for HICP inflation; IMF World Economic Outlook, 26 January 2021.

1) The ECB and Eurosystem staff macroeconomic projections report working day-adjusted annual growth rates, whereas the European Commission and the IMF report annual growth rates that are not adjusted for the number of working days per annum. Other forecasts do not specify whether they report working day-adjusted or non-working day-adjusted data. This table does not show ranges around the ECB staff projections. This reflects the fact that the standard computation of the ranges (based on historical projection errors) would not, in the present circumstances, provide a reliable indication of the unprecedented uncertainty surrounding the current projections. Instead, to better illustrate the current uncertainty, alternative scenarios based on different assumptions regarding the future evolution of the COVID-19 pandemic and the associated containment measures are provided in Section 5.

Box 4

Risks to the US and euro area outlook related to the American Rescue Plan

On 10 March 2021 the US Congress passed the Biden Administration’s American Rescue Plan, enacting, with some amendments, the first legislative priority of the new administration. The associated fiscal package is very bold, totalling USD 1.84 trillion (8.8% of 2020 GDP). The rescue plan is not included in the baseline projections, given the uncertainty with respect to its size, composition and timing that prevailed at the time of the cut-off date. This box provides a first assessment of the possible economic implications of the fiscal package on the US economy, as well as spillovers to the euro area based on model simulations.

The fiscal package aims to mitigate the economic consequences of the coronavirus pandemic and reboot the US economy. The package will include (i) a renewal of the unemployment benefit duration extension, (ii) an additional one-off pay-check to households, and (iii) an increase in both state and local spending to finance public health efforts and education. The scenario considered in the simulations is based on the package under discussion at the cut-off date (USD 1.9 trillion).[7] Although the package is frontloaded, as recent Congressional Budget Office estimates suggest, the simulations assume that both household and local and state governments would smooth its impact on the economy via higher savings and spending delays, in line with what was observed in the first round of stimulus last year.

The impact on the US economy depends on several key underlying assumptions. The government and local spending programmes have been modelled assuming an (temporary) increase in government consumption, and that the unemployment benefits and part of the pay-check affect targeted lump sum transfers to liquidity-constrained households, with the remaining pay-check stimulus taking the form of an increase in other lump sum transfers. In the model set-up, the Federal Reserve System accommodates fiscal expansion by holding interest rates constant for two years (broadly in line with current market expectations).[8]

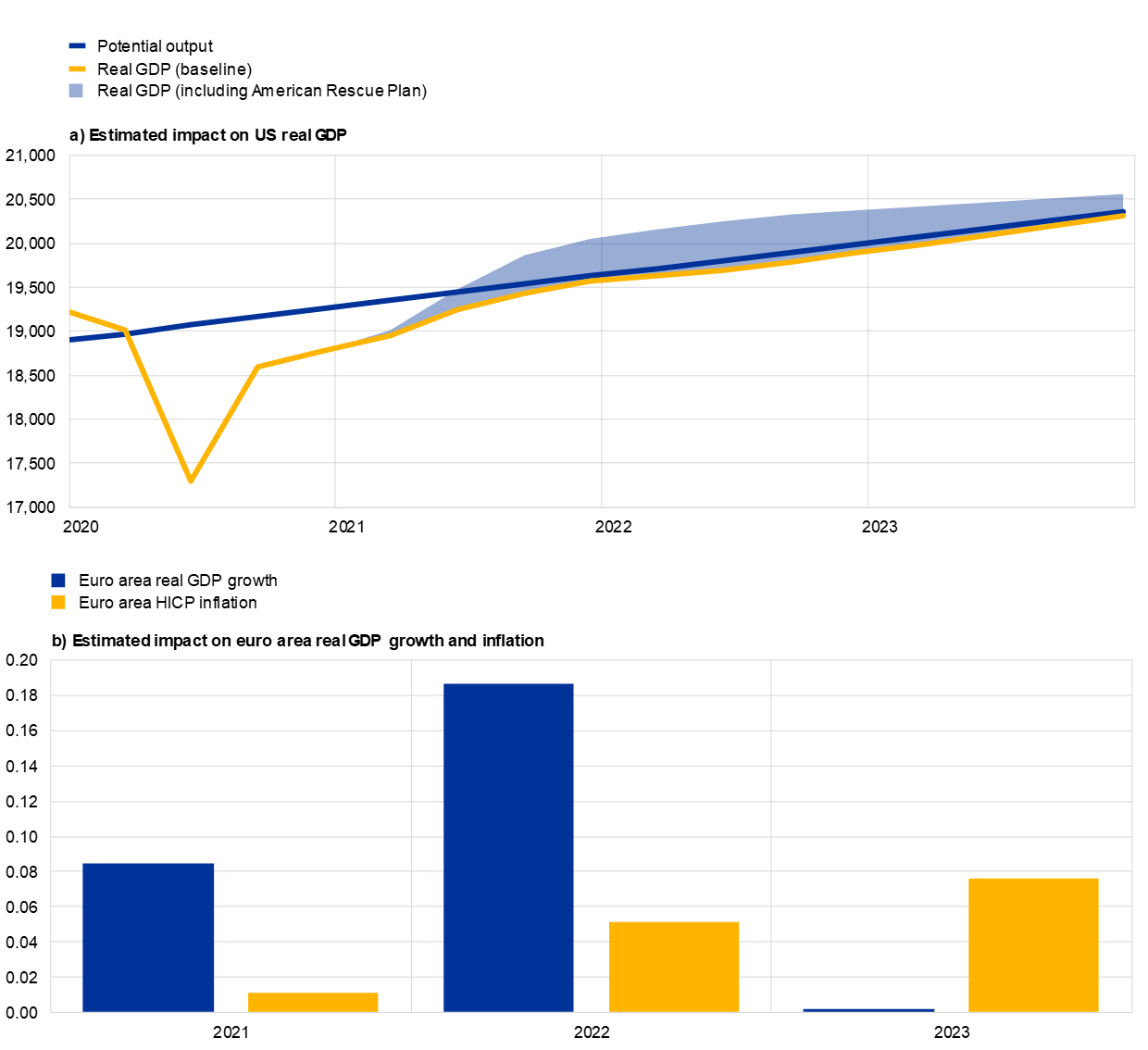

Model results suggest a significant boost to activity from the fiscal package, particularly in the near term. The fiscal stimulus boosts economic activity in the near term, as demand responds swiftly (see chart). Overall, compared with the current projection baseline[9], the additional fiscal stimulus would significantly raise the level of US real GDP over the projection horizon. As a result, the US economy could grow by 6.4% in 2021. Given the temporary nature of the fiscal stimulus, the effect vanishes over the projection horizon. In 2023 real GDP growth is expected to slow significantly.

Estimated impact on US real GDP and euro area real GDP and inflation

(quarterly; trillions of chained USD 2012 (chart a); impact on real GDP and HICP inflation in percentage points (chart b))

Sources: ECB calculations.

Notes: US results are informed using the Global Integrated Monetary and Fiscal model (GIMF), with no monetary policy reaction in 2021 or 2022, assuming a total package size of USD 1.9 trillion; they also include some judgement. Euro area simulations conducted with intra-euro area trade spillovers evaluate the impact of the changes to euro area foreign demand, competitors’ prices in domestic currencies, stock prices and a risk premium entering the credit spreads. Fiscal and monetary policies in the euro area are kept exogenous. The nominal short and long-term interest rates, nominal exchange rates and oil prices are assumed to remain unchanged. Euro area effects are computed using the ECB’s New Multi-Country Model, in which expectation formation is backward-looking with learning.[10]

Turning to inflation, the positive output gap is expected to translate into inflation pressures in 2022. Compared with the current projection baseline[11], the additional fiscal stimulus could raise US core personal consumption expenditure inflation by between 0.2 and 0.4 percentage points over the projection horizon. The temporary nature of the stimulus would diminish the positive output gap and inflationary pressures in 2023. The impact on inflation is based on the following assumptions: (i) a relatively flat Philipps curve, in line with recent experience; (ii) the cyclical position of the economy, which still has a negative output gap in the first half of 2021; and (iii) inflation expectations remaining anchored.[12] Nonetheless, there is uncertainty about the steepness of the Phillips curve, which represents an upside risk. At the same time, a strong pick-up in inflation could feed through to inflation expectations leading to unanchoring.

Given the size of the fiscal package, spillovers to the euro area could be notable. The New Multi-Country Model is used to gauge the effects of the American Rescue Plan package on the euro area.[13] Expectations of this fiscal package are to some degree already incorporated in the technical assumptions underlying the baseline projections.[14] The net economic effects on other countries depend on the strength of their linkages with the United States. First, an increase in US domestic demand increases US imports from abroad, thus positively affecting their GDP proportionally to their bilateral trade exposure. Second, the fiscal stimulus supports stock market valuations and lowers risk premia, particularly in the absence of monetary policy tightening. For the euro area, the additional impact of the US fiscal stimulus package, beyond what is assessed to be already included via the technical assumptions, is estimated to be an increase in euro area GDP of about 0.3% over the projection horizon, with a peak impact on growth rates of around 0.2 percentage points in 2022. The effects on HICP inflation are expected to be moderate, with a cumulative impact of about 0.15 percentage points over the projection horizon.

5 Alternative scenarios for the euro area economic outlook

As significant uncertainty about the future evolution of the COVID-19 pandemic and the degree of economic scarring persists, two scenarios, representing alternatives to the March 2021 ECB staff projections baseline, illustrate a range of plausible impacts of the COVID-19 pandemic on the euro area economy.

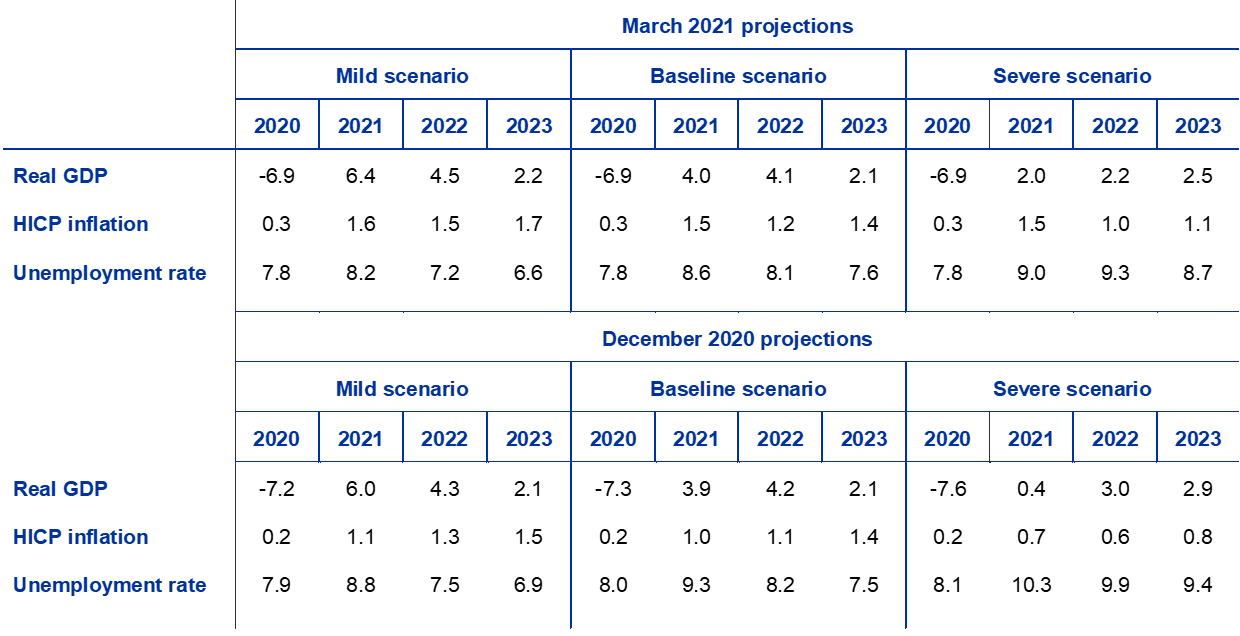

A mild scenario foresees a resolution of the health crisis by the end of 2021 and little longer-term scarring, while a severe scenario assumes a more protracted crisis and permanent losses in economic potential. Compared with the baseline, the mild scenario envisages a more rapid roll-out of vaccines, a higher degree of public acceptance and a higher level of vaccine effectiveness also towards virus mutations, which allow a swifter relaxation of containment measures, while more effective decisions taken by authorities and economic agents further limit the economic costs of containment measures. In contrast, the severe scenario envisages a strong intensification of the pandemic in the coming months with the emergence of virus mutations, which also imply a reduction in the effectiveness of vaccines, and maintenance of very stringent measures in the short term, albeit with limited results.[15] Containment measures continue to dampen activity significantly across sectors of the economy until medical solutions are successfully implemented. Successful implementation is assumed to occur by the end of 2021 in the mild scenario and by early 2022 in the baseline, whereas some containment measures are required until mid-2023 in the severe scenario. Compared with the baseline, the severe scenario features a more protracted negative economic impact of containment measures. This is amplified by increased insolvencies, which lead to credit frictions that adversely affect the borrowing costs of households and firms. At the same time, even in the severe scenario, monetary, fiscal and prudential policies are assumed to contain very severe financial amplification effects.

Table 2

Alternative macroeconomic scenarios for the euro area

(annual percentage changes, percentage of labour force)

The same broad narratives underlie the scenarios for the global economy and thus for euro area foreign demand. As a result of the high procyclicality of global trade with respect to global activity, at the end of 2023 euro area foreign demand would stand about 11% above its pre-crisis level in the mild scenario, while in the severe scenario it would just recover its pre-crisis level.

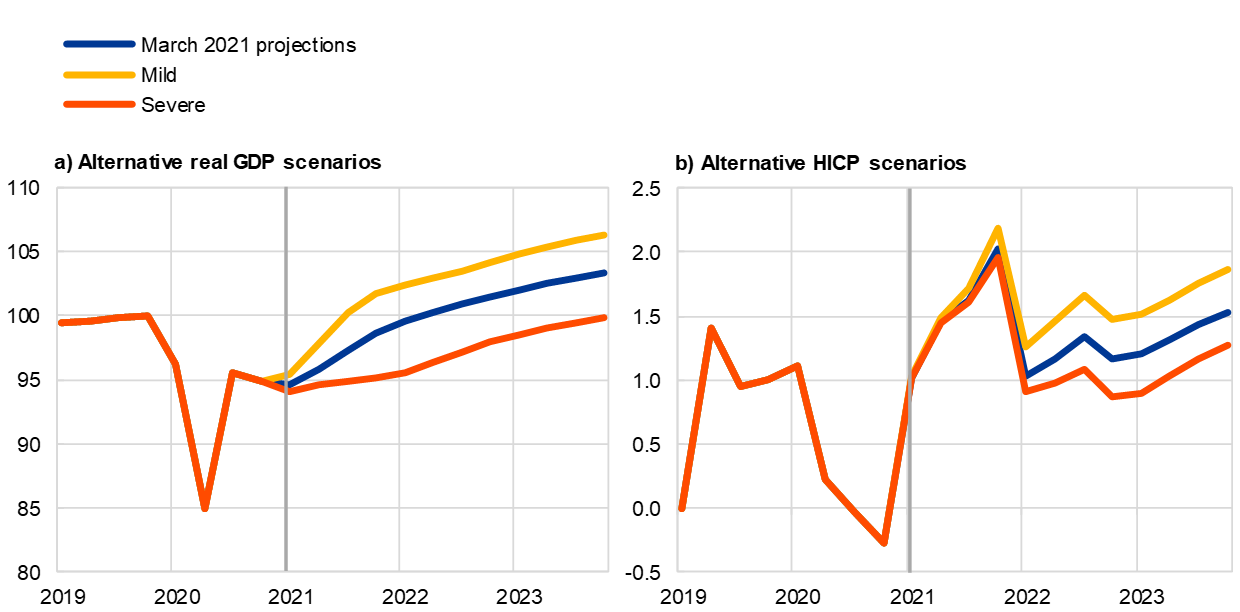

Real GDP would rebound strongly in the mild scenario, returning to its pre-crisis level as early as the third quarter of 2021, while in the severe scenario it would be approaching this level only in late 2023 (Chart 3). The mild scenario points towards a 0.4% increase in real GDP in the first quarter of 2021, followed by a notable rebound in the second quarter and further strengthening of economic activity during the rest of the year, triggered by the assumed swift roll-out of vaccines which instils confidence effects. As a result, economic activity returns to its pre-pandemic levels towards the end of 2021. The negative effects of the pandemic are projected to largely fade out by the end of 2022, when GDP returns to roughly the level envisaged in the pre-crisis December 2019 projections. In the severe scenario, economic activity would fall by 0.9% in the first quarter of 2021 and expand only modestly in the second quarter, before continuing its moderate recovery thereafter. Economic growth remains subdued in the severe scenario until early 2022, owing to the assumed further tightening of containment measures in the first quarter of 2021 and their relatively modest gradual relaxation thereafter. This outcome is further compounded by rather limited additional learning effects, significant ongoing uncertainty and financial amplification mechanisms, and only partly mitigated by policy support measures. A somewhat more vigorous growth recovery compared with the baseline is projected in the severe scenario only as of late 2022, given strong catch-up potential, which helps to make up almost all losses in real GDP, compared with the pre-crisis level, by the end of the projection horizon. The current scenarios are more symmetric around the baseline compared with the December 2020 projections.

Chart 3

Alternative scenarios for real GDP and HICP inflation in the euro area

(index: Q4 2019 = 100 (left-hand chart); annual percentage changes (right-hand chart))

Note: The vertical line indicates the start of the projection horizon.

Labour markets would recover in the mild scenario, as policies are largely successful in preventing hysteresis effects that are only partially contained in the severe scenario. In the mild scenario, the unemployment rate follows dynamics similar to those in the baseline, peaking in 2021 after the currently expected end of most of the government support measures and reverting quickly to its pre-crisis level in 2022. Conversely, in the severe scenario the unemployment rate does not return to the pre-crisis level recorded in the fourth quarter of 2019 and remains significantly elevated, reflecting higher reallocation needs across sectors. This highlights the upside risks related to possible bankruptcies and corporate vulnerabilities, as well as potential hysteresis.

HICP inflation would rebound in the short term in both scenarios, with more variations thereafter due to differences in the balance of supply and demand. This reflects that the key drivers of the pick-up in inflation in the baseline in the short term (namely the oil price assumptions, base effects in the energy component and the impact of the temporary VAT reduction in Germany) apply equally to the alternative scenarios. Beyond the short term, downward demand and upward supply effects on inflation are both expected to be larger in the severe scenario than in the mild scenario, but excess supply is envisaged to be higher in the severe scenario than in the mild one, depressing inflation. Nevertheless, compared with the December 2020 projections, the variations between scenarios have become notably smaller as the severe scenario now has a less pessimistic outlook.

Box 5

Sensitivity analysis

Projections rely heavily on technical assumptions regarding the evolution of certain key variables. Given that some of these variables can have a large impact on the projections for the euro area, examining the sensitivity of the latter to alternative paths of these underlying assumptions can help in the analysis of risks around the projections.

This sensitivity analysis aims to assess the implications of alternative oil price paths. The technical assumptions for oil price developments underlying the baseline, based on oil futures, predict a notably declining profile for oil prices, with the price per barrel of Brent crude oil falling by around 10% over the projection horizon. Two alternative paths of the oil price are analysed. The first is based on the 25th percentile of the distribution provided by the option-implied densities for the oil price on 16 February 2021, which is the cut-off date for the technical assumptions. This path implies a gradual decrease in the oil price to USD 41.1 per barrel in 2023, which is 23.4% below the baseline assumption for that year. Using the average of the results from a number of staff macroeconomic models, this path would have a small upward impact on real GDP growth (around 0.1 percentage points in 2022 and 2023), while HICP inflation would be 0.2 percentage points lower in 2021, 0.4 percentage points lower in 2022 and 0.3 percentage points lower in 2023. The second path is based on the 75th percentile of the same distribution and implies an increase in the oil price to USD 70 per barrel in 2023, which is 30.4% above the baseline assumption for that year. This path would entail HICP inflation being 0.2 percentage points higher in 2021 and 0.4 percentage points higher in both 2022 and 2023, while real GDP growth would be slightly lower (by 0.1 percentage points in 2022 and in 2023).

© European Central Bank, 2021

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary (available in English only).

PDF ISSN 2529-4466, QB-CE-21-001-EN-N

HTML ISSN 2529-4466, QB-CE-21-001-EN-Q

- The cut-off date for technical assumptions, such as those for oil prices and exchange rates, was 16 February 2021 (Box 1). The macroeconomic projections for the euro area were finalised on 24 February 2021. The current macroeconomic projection exercise covers the period 2021-23. Projections over such a long horizon are subject to very high uncertainty, and this should be borne in mind when interpreting them. See the article entitled “An assessment of Eurosystem staff macroeconomic projections” in the May 2013 issue of the ECB’s Monthly Bulletin. See http://www.ecb.europa.eu/pub/projections/html/index.en.html for an accessible version of the data underlying selected tables and charts.

- The assumption for euro area ten-year nominal government bond yields is based on the weighted average of countries’ ten-year benchmark bond yields, weighted by annual GDP figures and extended by the forward path derived from the ECB’s euro area all-bonds ten-year par yield, with the initial discrepancy between the two series kept constant over the projection horizon. The spreads between country-specific government bond yields and the corresponding euro area average are assumed to be constant over the projection horizon.

- Estimated at around ½% of GDP over 2021-23 and broadly unchanged from the December 2020 projections.

- The fiscal policy stance is measured as the change in the cyclically adjusted primary balance net of government support to the financial sector and is also adjusted for the impact of NGEU grants.

- On the basis of constant (2020) weights, the outcome for HICP excluding energy and food in January 2021 is estimated by the ECB to have been 1.0%, compared with the official outcome of 1.4% published by Eurostat (calculated using 2021 weights).

- The March 2021 ECB staff projections are based on constant weights for the projection horizon, implying some additional uncertainty regarding the inflation projections in 2022 and 2023.

- The simulated package was USD 1.9 trillion in line with the initial proposals. Following amendments in Congress, the latest Congressional Budget Office calculations suggest that the package size will be USD 1.84 trillion.

- The effects on the US economy are estimated using the Global Integrated Monetary and Fiscal (GIMF) Model (see Anderson et al., “Getting to Know GIMF: The Simulation Properties of the Global Integrated Monetary and Fiscal Model”, Working Paper, No 13/55, IMF, 2013) combined with judgement. The magnitudes of fiscal multipliers are subject to high uncertainty. In the GIMF model, the implied fiscal multipliers (in the first year) are 1.0 for government spending, 0.7 for transfers to liquidity-constrained households and 0.3 for general transfers (under the modelling assumption of no monetary policy reaction). While these multipliers are broadly in line with the academic literature, there is also some empirical evidence that fiscal multipliers are asymmetric and state dependent: they have been found to depend on the direction of the fiscal action (smaller if the policy is expansionary) and on the state of the economy (larger in recessions than in expansions).

- The current baseline projects real GDP growth in the US of 4.8%, 2.3% and 2% for 2021, 2022 and 2023 respectively.

- Dieppe et al., “The ECB's New Multi-Country Model for the euro area: NMCM – with boundedly rational learning expectations”, Working Paper Series, No 1316, ECB, Frankfurt am Main, April 2011.

- The current baseline projects core personal consumption expenditure inflation in the US at 1.8%, 2.1% and 2% for 2021, 2022 and 2023 respectively.

- The effects on inflation are sensitive to model specifications and the degree to which agents are assumed to perfect foresight or form expectations via learning or are backward looking. The increase in inflation is estimated to be around 0.2 percentage points per 1% closure of the output gap.

- Spillovers from the United States to non-euro area countries (thereby affecting spillovers to the euro area) were assessed using the ECB-Global model (Georgiadis, G. et al., “ECB-Global 2.0: a global macroeconomic model with dominant-currency pricing, tariffs and trade diversion”, Working Paper Series, No 2530, ECB, Frankfurt am Main, March 2021).

- Since the announcement of the package proposal, bond yields, equities and oil prices have all increased, although that reflects a host of other factors, including an improving global growth outlook amid more positive pandemic prospects. The stance taken by monetary authorities in response to the fiscal expansion is also key. As monetary policy rates are assumed to remain unchanged throughout 2021 and 2022, changes in the US dollar vis-à-vis the euro are also assumed to be limited.

- Given difficulties to predict further intensifications of the pandemic, the projections take the possibility of a resurgence of the virus into account by distributing the economic impacts over the period until the health crisis is resolved.

- 11 March 2021