On the interaction between different bank liquidity requirements

The post-crisis regulatory framework introduced multiple requirements on banks’ capital and liquidity positions, sparking a discussion among policymakers and academics on how the various requirements interact with one another. This article contributes to the discussion on the interaction of different regulatory metrics by empirically examining the interaction between the liquidity coverage ratio (LCR) and the net stable funding ratio (NSFR) for banks in the euro area. The findings suggest that the two liquidity requirements are complementary and constrain different types of banks in different ways, similarly to the risk-based and leverage ratio requirements in the capital framework. This dispels claims that the LCR and the NSFR are redundant and underlines the need for a faithful and consistent implementation of both measures (and the entire Basel III package more broadly) across all major jurisdictions, to maintain a level playing field at the global level and to ensure that the post-crisis regulatory framework delivers on its objectives.

1 Introduction

The post-crisis regulatory framework introduced multiple requirements on banks’ capital and liquidity positions, sparking a discussion among policymakers and academics on how the various requirements interact with one another. The 2010 Basel III reforms introduced the leverage ratio as a supplementary measure to the risk-based capital requirements, as well as the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) requirements to capture liquidity risks. With multiple requirements applicable in parallel, the new framework has led to some discussion on the interaction of the various metrics.[1]

This article contributes to the discussion on the interaction of different regulatory metrics by empirically examining the interaction between the LCR and the NSFR for banks in the euro area. Both the LCR and the NSFR were included in the December 2010 Basel III agreement, in which the Basel Committee on Banking Supervision (BCBS) noted that the standards were meant to achieve two separate but complementary objectives.[2] While the LCR became applicable in 2014, the BCBS agreed on a rigorous review process for the NSFR and its implications for financial market functioning and the economy, delaying its applicability as a minimum standard until 2018. Following this agreement, there has been some discussion – both among policymakers and academics – on whether the two requirements are indeed complementary, and whether both of them are needed to ensure sound liquidity profiles and management. Our article contributes to this debate by making use of granular supervisory data for euro area banks and the theoretical framework developed by Cecchetti and Kashyap (2018).

The findings suggest that the two liquidity requirements are indeed complementary and constrain different types of banks in different ways, similarly to the risk-based and leverage ratio requirements in the capital framework. While the two liquidity ratios are positively correlated, there is no evidence of a mechanical interaction between them since movement in one ratio does not necessarily imply movement in the other. Moreover, their relative tightness depends on the composition of each bank’s balance sheet, with significant differences across business models. In other words, the two different types of requirements are binding on different types of banks, depending on the risk profile of their liquidity positions. Both requirements thus complement each other and are needed to address liquidity risks in the banking sector. This is similar to the capital framework, where the relative tightness of the risk-based requirements and the leverage ratio depends on the composition of a bank’s assets and the two measures complement each other in capturing banks with different risk profiles. However, a key difference is that, while the leverage ratio and the risk-based requirements have essentially the same objective (ensuring an adequate level of resilience), with the former acting as a backstop for the latter, the objectives of the LCR and the NSFR are complementary but different in nature.

2 Regulatory requirements on bank liquidity: the LCR and the NSFR

While strong capital positions are a necessary condition to guarantee the stability of the banking sector, the global financial crisis of 2007‑08 has shown that they are by themselves insufficient and need to be complemented by sound liquidity standards. During the early phases of the global financial crisis, funding liquidity evaporated and many banks experienced difficulties despite still adequate capital levels (see, for example, Brunnermeier, 2009). To address this issue, the BCBS developed its Principles for Sound Liquidity Risk Management and Supervision[3] and complemented them with two minimum standards for funding liquidity with separate but complementary objectives: the LCR and the NSFR (see, for example, Basel Committee on Banking Supervision, 2010).

The objective of the LCR is to promote short-term resilience of a bank's funding profile by ensuring that it has sufficient liquid assets to cover possible short-term liquidity outflows. In particular, the LCR specifies that a bank needs to have “an adequate stock of unencumbered high-quality liquid assets (HQLA) that can be converted into cash easily and immediately in private markets to meet its liquidity needs for a 30‑calendar day liquidity stress scenario” (for details see, for example, Basel Committee on Banking Supervision, 2013). Liquidity needs over the 30‑day period are calculated by multiplying outstanding balances of various types of liabilities and off-balance sheet commitments by the rates at which they are expected to be drawn down in a stress scenario, and are netted (subject to a cap) with expected liquidity inflows over the same period to calculate net liquidity outflows.

The NSFR objective is complementary to the LCR in that it aims to ensure funding resilience over a longer time horizon, requiring banks to fund long-term assets with long-term liabilities and thus limit the degree of maturity mismatch. Specifically, the NSFR requires that banks’ available stable funding over a one-year horizon is at least as large as the required stable funding over the same horizon, where available stable funding and required stable funding are defined as weighted fractions of liabilities and assets respectively, as well as off-balance sheet items (for details, see, for example, Basel Committee on Banking Supervision, 2014). The NSFR aims to prevent banks from excessively financing long-term assets with short-term liabilities and thus seeks to mitigate the potential for future funding stress. While the NSFR has thus far not been a binding requirement in the European Union, it has been implemented via the revised version of the Capital Requirements Regulation (CRR) published in June 2019 and will be applicable as of 28 June 2021.

While there is broad agreement on the necessity of complementing regulatory capital with liquidity standards, there has recently been some discussion on whether both the LCR and the NSFR are needed. Using a simplified version of a bank’s balance sheet, Cecchetti and Kashyap (2018) (hereafter the “CK framework”) argue that the two types of requirements will almost surely never bind at the same time and may be treated as substitutes of each other. Specifically, they divide assets into liquid, illiquid and other assets, and liabilities into runnable, stable and other liabilities, and illustrate that the relative tightness of the LCR and the NSFR depends on the relative importance of other assets and other liabilities (see Box 1 for a more detailed discussion). Using a sample of UK banks, they show that the relative importance of other assets and other liabilities tends to be such that the LCR is the tighter constraint, which leads them to conclude that only one of the requirements is needed.

Box 1

Implications of the Cecchetti and Kashyap (2018) framework [4]

Overview of the CK framework

Cecchetti and Kashyap (2018) use a stylised bank balance sheet, where assets comprise liquid (H), illiquid (I) and other (OA) assets, while liabilities comprise runnable (R), stable (S) and other (OL) liabilities. In addition, they assume that banks have off-balance sheet exposures that affect both the LCR and the NSFR (OBSL and OBSN respectively).

Table A

Simplified bank balance sheet for liquidity requirements

Notes: Stylised bank balance adopted from Cecchetti and Kashyap (2018). Off-balance sheet exposures (OBSL and OBSN) are not represented.

In this simplified framework, the two requirements can be written as:

(1)

(2)

Using the balance sheet identity and rearranging terms, they can be expressed as follows:

(3)

(4)

Subtracting surplus liquid assets (3) from surplus stable funding (4) defines what is labelled as net other positions (NOP):

(5)

If NOP > 0, the amount of surplus stable funding (i.e. the amount of stable liabilities that the bank has on top of the amount that is needed to fulfil the NSFR requirement) will be larger than the amount of surplus liquid assets (i.e. the amount of liquid assets that the bank has on top of the amount that is needed to fulfil the LCR requirement), and if NOP < 0 the reverse is true. This trivially implies that when NOP > 0, a bank that meets the LCR also meets the NSFR and, conversely, if NOP < 0, a bank that meets the NSFR also meets the LCR.

In a final step, Cecchetti and Kashyap (2018) show that for a set of UK universal banks and building societies, NOP tends to be larger than zero. They conclude from this that banks meeting the LCR requirement will very likely meet the NSFR requirement as well, that one of the requirements is implicitly defining the other one as a shadow measure, and that consequently only one liquidity requirement is needed.

Implications of the CK framework

Before empirically testing the assertions of the CK framework, it is useful to spell out clearly what the theoretical framework does and does not imply.

First, as noted above, the framework implies that when NOP>0, a bank that meets the LCR also meets the NSFR. However, it does not imply that when a bank meets the LCR, then NOP>0. There can obviously be cases in which NOP<0, and in these cases a bank meeting the LCR may or may not meet the NSFR. The reverse logic applies to the opposite case: if NOP>0, a bank meeting the NSFR may or may not meet the LCR. More generally, the framework specifies that, depending on whether NOP is larger or smaller than zero, either surplus liquid assets will be larger than surplus stable funding, or vice versa. However, it does not make any theoretical predictions on the sign of NOP, which is instead an empirical question and may vary both across banks and over time.

Second, the framework allows deriving statements on the relative amounts of surplus liquid assets and surplus stable funding, but does not allow similar statements to be derived for the relative size of liquidity coverage and net stable funding ratios. The reason for this is that, as we will show below, the denominators of the LCR and the NSFR tend to correspond to very different fractions of a bank’s balance sheet, so that a similar amount of surplus can still imply large differences between the LCR and the NSFR in ratios. To illustrate this, consider a bank with zero off-balance sheet exposures and the balance sheet shown in Table B.

Table B

Simplified bank balance sheet for liquidity requirements amended with actual numbers

Notes: Stylised bank balance adopted from Cecchetti and Kashyap (2018). Off-balance sheet exposures (OBSL and OBSN) are assumed to be zero.

In this case, NOP>0 holds (since OA>OL), surplus stable funding is larger than surplus liquid assets (as predicted by the framework), but at the same time the NSFR is considerably smaller (and thus, many would argue, “tighter”) than the LCR (1.13 and 2 respectively). Put differently: the statement that when NOP>0, a bank that meets the LCR also meets the NSFR is true, but it does not imply that when NOP>0 the LCR will be “tighter” or “less slack” than the NSFR.

Finally, in the theoretical framework the two ratios are not necessarily shadow measures of each other (in the sense that changes in one of them automatically imply changes in the other). To see this, consider the slightly modified balance sheet shown in Table C.

Table C

Simplified bank balance sheet for liquidity requirements with modified actual numbers

Notes: Stylised bank balance adopted from Cecchetti and Kashyap (2018). Off-balance sheet exposures (OBSL and OBSN) are assumed to be zero.

The only difference in Table C relative to Table B is a reshuffling of five units of liquid assets into other assets. This reshuffling implies a significant change in the LCR, which is reduced from 2 to 1, while the NSFR is left unchanged. This illustrates that the LCR and the NSFR are shadow measures of each other only to the extent that changes in their components are uncorrelated with changes in other assets or other liabilities. In Section 3.2 we investigate empirically whether this is the case.3

Empirical analysis

3.1 Data and descriptive statistics

The empirical analysis in this article is based on bank group-level supervisory data that includes information on 224 banks in Europe’s Single Supervisory Mechanism (SSM). The sample is composed of 94 significant institutions (SIs) directly supervised by the ECB and 130 high-priority less significant institutions (LSIs) that are supervised by national authorities forming part of the SSM framework. The data is reported by banks using COREP and FINREP templates and spans the period from the first quarter of 2015 to the fourth quarter of 2017.

All banks in the sample meet the minimum LCR requirement, but not all banks meet the NSFR requirement. This may reflect the fact that the NSFR requirement is not yet binding and banks could still be in the process of adjusting to this forthcoming requirement. The average LCR for the banks in our sample is 2.7, considerably higher than the average NSFR of 1.3 (see Table 1). In addition, the distribution of the LCR is highly dispersed, as indicated by both the standard deviation and the maximum and minimum values.

Table 1

Distribution of LCR and NSFR

Sources: COREP and authors’ calculations.

Notes: Minimum LCR requirement: 1; minimum NSFR requirement: 1.

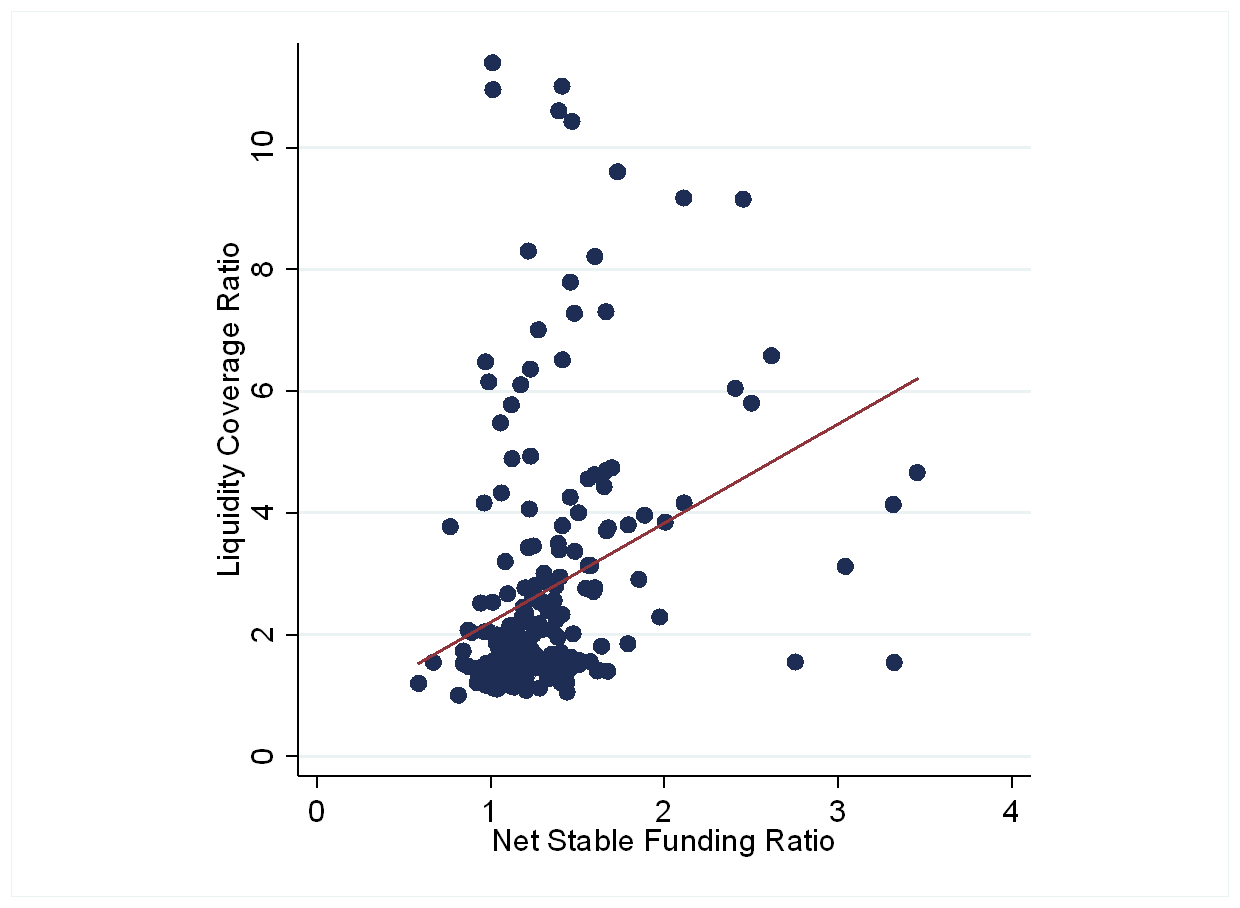

The two liquidity ratios are positively correlated, but the wide dispersion does not suggest a strong mechanical interaction between the two measures. Chart 1 shows a scatterplot of each bank’s LCR and NSFR for the fourth quarter of 2017. The correlation between the two ratios is positive and statistically significant. However, there is significant dispersion, which appears inconsistent with a strong mechanical interaction.

Chart 1

LCR and NSFR for the sample of banks

(x-axis: NSFR ratio; y-axis: LCR ratio)

Sources: COREP and authors’ calculations.

Note: This chart is based on information for the fourth quarter of 2017.

To empirically examine the interaction between LCR and NSFR, we use the bank-level data to construct the measures of surplus liquid assets, surplus stable funding and net other positions as described in Box 1. We reconstruct the stylised balance sheet of the CK framework by using granular information on the composition of banks’ assets and liabilities, and the relative weights that each item receives in the LCR and the NSFR. Surplus stable funding is the amount of stable liabilities in excess of the minimum amount required to fulfil the NSFR requirement, while surplus liquid assets is the amount of liquid assets in excess of the minimum amount required to fulfil the LCR requirement. Finally, net other positions (NOP) is the sum of other assets and off-balance sheet exposures that affect the LCR, minus other liabilities and off-balance sheet exposures that affect the NSFR (see Box 1 for details).

3.2 Examining the interaction between LCR and NSFR

Chart 2 shows that – depending on the sign of NOP – either surplus liquid assets will be larger than surplus stable funding, or vice versa. If surplus liquid assets are plotted against surplus stable funding (as defined in Section 3.1), the resulting chart shows that the latter is larger than the former for banks with NOP > 0 (blue dots). For these banks, meeting the LCR automatically implies also meeting the NSFR (since surplus stable funding > surplus liquid assets > 0). Conversely, for banks with NOP < 0 (red dots), surplus liquid assets are larger than surplus stable funding, implying that if these banks meet the NSFR they necessarily also meet the LCR (since surplus liquid assets > surplus stable funding > 0). Overall, the data confirm the theoretical prediction of the CK framework that the relative magnitude of surplus liquid assets and surplus stable funding depends on the sign of NOP (see Box 1).

The data further show that the sign of NOP is not uniform but varies considerably across banks, implying that no single liquidity constraint will be the tightest one across all banks. As shown in Chart 2, about one-third of the banks in our sample have NOP < 0 and thus surplus stable funding smaller than surplus liquid assets (red dots). This contrasts with the CK assertion that banks’ balance sheets are generally such that NOP > 0 and therefore that banks meeting the LCR are very likely also to meet the NSFR. In fact, at the very left of the chart there are several banks that meet the LCR (surplus liquid assets > 0) but do not meet the NSFR (surplus stable funding < 0).

Chart 2

Surplus liquid assets and surplus stable funding

(x-axis: surplus stable funding; y-axis: surplus liquid assets)

Sources: COREP and authors’ calculations.

Note: This chart is based on information for the fourth quarter of 2017.

The findings suggest that the two ratios are complementary and that their relative tightness depends on the composition of each bank’s balance sheet. Whether one requirement is slack or not when the other requirement is binding depends on the relative importance of the different asset and liability classes. Since each liquidity ratio captures different types of risks, the requirements will constrain different types of banks in different ways, depending on their business models. This is similar to the capital framework, where different capital ratios are the binding constraint for different types of banks. However, a key difference is that, while the leverage ratio and the risk-based requirements have essentially the same objective (ensuring an adequate level of resilience), with the leverage ratio acting as a backstop, the objectives of the LCR and the NSFR are complementary but different in nature, as explained in Section 2.

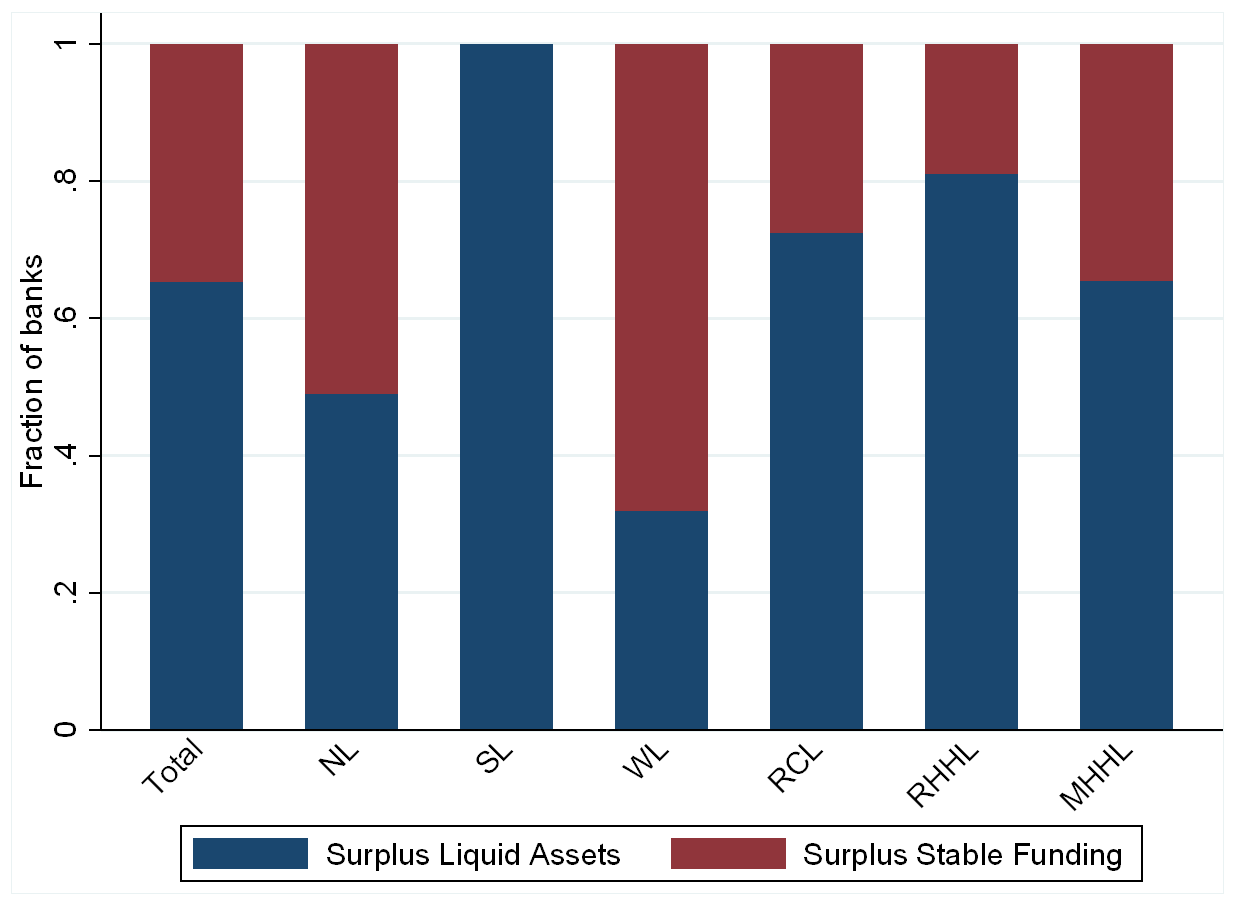

Chart 3 shows that surplus stable funding tends to be smaller than surplus liquid assets for non-lenders and wholesale lenders, while the reverse is true for banks with other business models.[5] The relative amounts of surplus liquid assets and surplus stable funding tend to vary substantially across banks, depending, for example, on the banks’ business models. The majority of banks have a lower surplus in terms of liquid assets, with the exception of non-lenders (banks for which other business activities, such as asset management, trading or insurance, are important relative to lending) and wholesale lenders, who tend to be more constrained in terms of stable funding. A possible reason for this is that retail-based funding is treated relatively favourably in the NSFR, benefiting banks that rely on this type of funding compared with those that rely more on wholesale funding. In any case, the chart strengthens the argument that the two measures are complementary, with each of them being more binding for different types of banks.

Chart 3

Fraction of banks for which surplus liquid assets and surplus stable funding is smaller, by business model

Sources: COREP and authors’ calculations.

Notes: The first bar refers to the total sample of banks in the first quarter of 2017. The remaining bars show a breakdown by business model, where categories include non-lenders (NL), small lenders (SL), wholesale lenders (WL), retail-funded corporate lenders (RCL), retail-funded household lenders (RHHL), and mix-funded household lenders (MHHL).

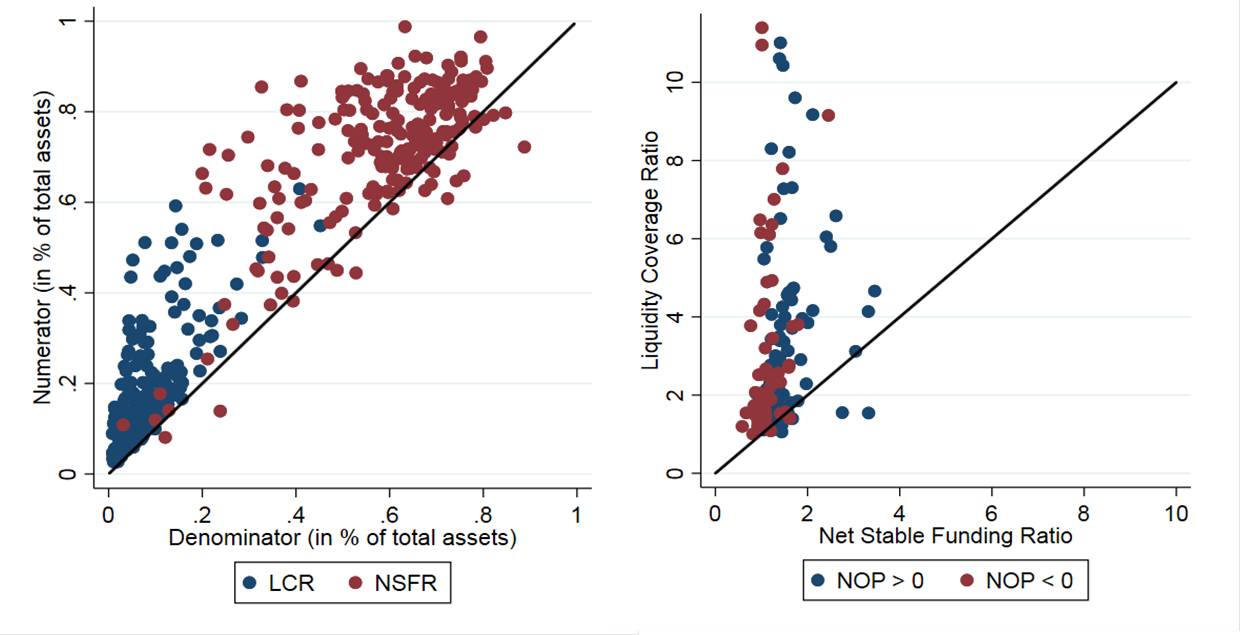

While this study has so far compared surplus liquid assets with surplus stable funding, the relative tightness of the two liquidity ratios also depends on the magnitude of their numerators and denominators with respect to the total balance sheet. The left-hand panel in Chart 4 shows that the elements of the balance sheet used for the calculation of the LCR tend to correspond to a significantly smaller portion of the total balance sheet than the elements used for the NSFR. For the vast majority of banks, the LCR numerator and denominator correspond to 20% or less of the total balance sheet, whereas for the NSFR the numbers are centred between 75 and 80%. As explained in Box 1, this implies that a bank for which the amounts of surplus liquid assets and surplus stable funding are roughly similar may still have a significantly higher LCR than NSFR.

Using actual ratios rather than surplus measures, the right-hand panel in Chart 4 shows that the LCR tends to be larger (i.e. slacker) for the vast majority of banks in our sample, irrespective of whether net other positions are greater or smaller than zero. Although many banks tend to have a smaller amount of surplus liquid assets than surplus stable funding (the blue dots in Chart 2), the LCR numerators and denominators correspond to a significantly smaller portion of the balance sheet, so that the smaller surplus still implies a considerably higher LCR for these banks (compared with the NSFR). This is irrespective of the sign of NOP, which allows making predictions only on the relative magnitude of the two surplus measures. Whether it is more useful to compare surplus measures or ratios when assessing the relative tightness of the liquidity measures is a conceptual question that does not have a definite answer. Intuitively, one could argue that banks might need larger surpluses as buffers in cases where larger fractions of their balance sheets are at risk, which would speak in favour of looking at ratios rather than absolute amounts.[6] Moreover, if banks manage their liquidity requirements by targeting buffers above the required liquidity ratios, then the surplus measures and the use of the sign of NOP may be less informative in understanding banks’ behaviour. Importantly, the fact that the LCR tends to be higher than the NSFR does not imply that only the NSFR is needed, since the two ratios address different types of risks (see Section 2). As we will show below, the ratios cannot be regarded as substitutes of each other; rather, both of them are needed to address these different types of risk.

Chart 4

LCR and NSFR

(left-hand panel: x-axis: denominator of the ratios; y-axis: numerator of the ratios; right-hand panel: x-axis: NSFR; y-axis: LCR)

Sources: COREP and authors’ calculations.

Note: This chart is based on information for the fourth quarter of 2017.

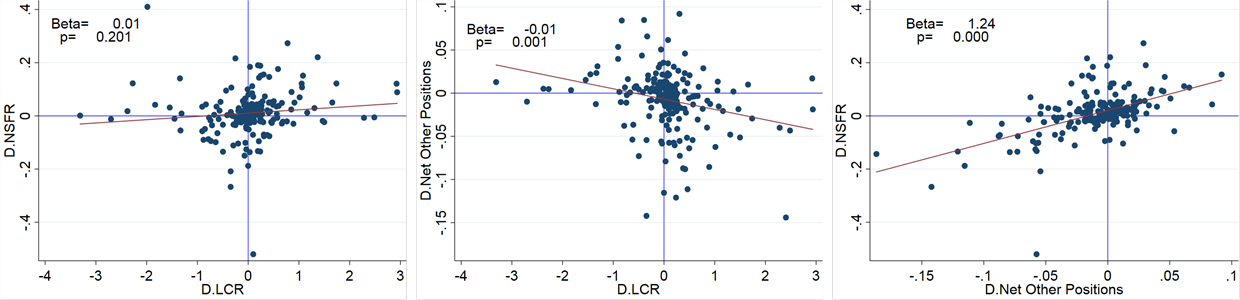

While there is co-movement between the LCR and the NSFR, movement in one ratio does not automatically imply movement in the other, and therefore the two requirements are not shadow measures of each other. As explained in Box 1, the extent to which movements in one of the liquidity measures imply movements in the other depends on how these movements correlate with changes in NOP. Chart 5 shows that NOP changes both over time and in correlation with changes in surplus liquid assets and surplus stable funding. For example, the co-movement between surplus stable funding and NOP is stronger than the co-movement between surplus liquid assets and surplus stable funding (see Panel A). This also holds in terms of ratios, where the co-movement between LCR and NSFR is not statistically significant, while there is significant co-movement between NOP and the two ratios (see Panel B). Overall, the chart shows that movements in the NSFR do not automatically imply movements in the LCR and that the interaction between the LCR and the NSFR may also change over time, since NOP is not static. In other words: a given LCR does not imply a ‘shadow’ NSFR, so that the two measures should not be regarded as substitutes of each other and are therefore not redundant.

Chart 5

Co-movement between LCR, NSFR and other assets and liabilities

PANEL A – Surplus measures

PANEL B – Ratios

Sources: COREP and authors’ calculations.

Note: This chart is based on information for the fourth quarter of 2017.

4 Conclusion

This article empirically examines the interaction between the LCR and the NSFR for a sample of euro area banks. The results suggest that the two requirements are complementary and should not be regarded as shadow measures of each other. While the two liquidity ratios are positively correlated, there is no evidence of a mechanical interaction between them since movement in one ratio does not necessarily imply movement in the other. Moreover, their relative tightness depends on the composition of each bank’s balance sheet and the requirements constrain different types of banks in different ways, with significant differences across business models. This suggests that both requirements are needed to fully address liquidity risks in the banking sector, as they have different objectives and are meant to capture different types of risks.

Faithful and consistent implementation of both liquidity requirements across jurisdictions is needed to foster sound liquidity risk management, and ensure financial stability and a global level playing field for banks. While the LCR has already been implemented in all major regions, the process for implementing the NSFR has not been initiated in all relevant jurisdictions. The findings in this article illustrate that the LCR and the NSFR are complementary, constraining banks with different liquidity risk profiles in different ways. This underlines the need for a faithful and consistent implementation of both measures (and the entire Basel III package more broadly) across all major jurisdictions, to maintain a level playing field at the global level and to ensure that the post-crisis regulatory framework delivers on its objectives.

5 References

Basel Committee on Banking Supervision, “Basel III: A global framework for more resilient banks and banking systems”, Bank for International Settlements, Basel, Switzerland, 2010.

Basel Committee on Banking Supervision, “Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools”, Bank for International Settlements, Basel, Switzerland, 2013.

Basel Committee on Banking Supervision, “Basel III: the net stable funding ratio”, Bank for International Settlements, Basel, 2014.

Behn, M., Daminato, C. and Salleo, C., “A dynamic model of bank behaviour under multiple regulatory constraints”, Working Paper Series, No 2233, ECB, Frankfurt am Main, January 2019.

Brunnermeier, M., “Deciphering the Liquidity and Credit Crunch 2007‑2008”, Journal of Economic Perspectives, Vol. 23(1), pp. 77‑100, 2009.

Cecchetti, S. and Kashyap, A., “What Binds? Interactions between Bank Capital and Liquidity Regulations” Working Paper, Brandeis International Business School and Chicago Booth School of Business, 2016.

Cecchetti, S. and Kashyap, A., “Inspecting Basel III”, Working Paper, Brandeis International Business School and Chicago Booth School of Business, 2018.

Cecchetti, S. and Schoenholtz, K., “Regulatory Reform: a scorecard”, CEPR Discussion Paper Series on International Macroeconomics and Finance, No 12465, 2017.

Chami, R., Cosimano, T., Ma, J. and Rochon, C., “What's Different about Bank Holding Companies?”, IMF Working Papers, No 17/26, February 2017.

Goel, T., Lewrick, U., and Tarashev, N. (2017). “Bank capital allocation under multiple constraints”, BIS Working Papers, No 666, Bank for International Settlements, Basel, 2017.

Hoerova, M., Mendicino, C., Nikolov, K., Schepens, G., and Van den Heuvel, S., “Benefits and costs of liquidity regulation”, Working Paper Series, No 2169, ECB, Frankfurt am Main, July 2018.

Mankart, J., Michaelides, A. and Pagratis, S., “Bank capital buffers in a dynamic model”, Financial Management, September 2018.

- Recent papers studying the interaction between different capital requirements include Goel et al. (2017) and Mankart et al. (2018). The interaction between capital and liquidity requirements is studied by Chami et al. (2017), Cecchetti and Kashyap (2018), Hoerova et al. (2018) and Behn et al. (2019).

- For further details see Basel Committee on Banking Supervision (2010). The LCR aims to “promote short-term resilience of a bank’s liquidity risk profile by ensuring that it has sufficient high-quality liquid resources to survive an acute stress scenario lasting for one month.” In contrast, the NSFR takes a longer-term perspective and aims to create “additional incentives for a bank to fund its activities with more stable sources of funding on an ongoing structural basis.”

- Available here.

- See also Cecchetti and Kashyap (2016) and Cecchetti and Schoenholtz (2017).

- The business model classification is broadly based on existing methodologies (ECB Banking Supervision, Centre for European Policy Studies) and aims to include banks that are similar along some core characteristics. Accordingly, the sample comprises 52 non-lenders (banks whose other business activities, such as asset management, trading or insurance, are important relative to lending), 10 small lenders (small banks whose lending is the main business activity), 25 wholesale lenders (banks whose lending is the main business activity, predominantly to credit institutions and corporations and funded through the wholesale market), 29 retail-funded corporate lenders (banks whose lending is the main business activity, predominantly to credit institutions and corporations and funded mostly by retail clients), 74 retail-funded household lenders (banks whose lending is the main business activity, predominantly to households and funded mostly by retail clients), and 30 mix-funded household lenders (banks whose lending is the main business activity, predominantly to households and funded mostly through the wholesale market), plus 4 banks for which the data required for business model classification were not available.

- As an intuitive example, let us assume that bank A and bank B both have surplus liquid assets amounting to 5% of total assets. If bank A has runnable liabilities amounting to 50% of assets and bank B has runnable liabilities amounting to 10% of assets, one would likely argue that bank B has more slack in terms of liquidity. This would be reflected in the LCRs of the two banks (55/50 = 1.1 for bank A and 15/10=1.5 for bank B), but not in the amounts of surplus liquid assets (5% of assets for both banks).