Understanding what happens when “angels fall”

Published as part of the Financial Stability Review, November 2020.

Credit rating downgrades especially from investment grade to high yield (“fallen angels”) can adversely affect the price and ease of a firm’s debt issuance. Credit rating agencies (CRAs) assess whether an issuer and its debt are relatively safe “investment grade” (rated BBB- or above) or more risky “high yield” (rated BB+ or below). In this context, a fallen angel is generally understood to be an issuer that has been downgraded from investment grade to high yield by at least one of the three major CRAs. Such a downgrade can force (institutional) investors to sell securities, as investment mandates may restrict the securities that they are allowed to hold.[1] It may also trigger a sharp increase in a firm’s cost of bond financing and reduce its market access. This box considers the prospects for fallen angels, and assesses whether the consequences for market access and the risk of downgrade-linked sell-offs are as great as sometimes feared.

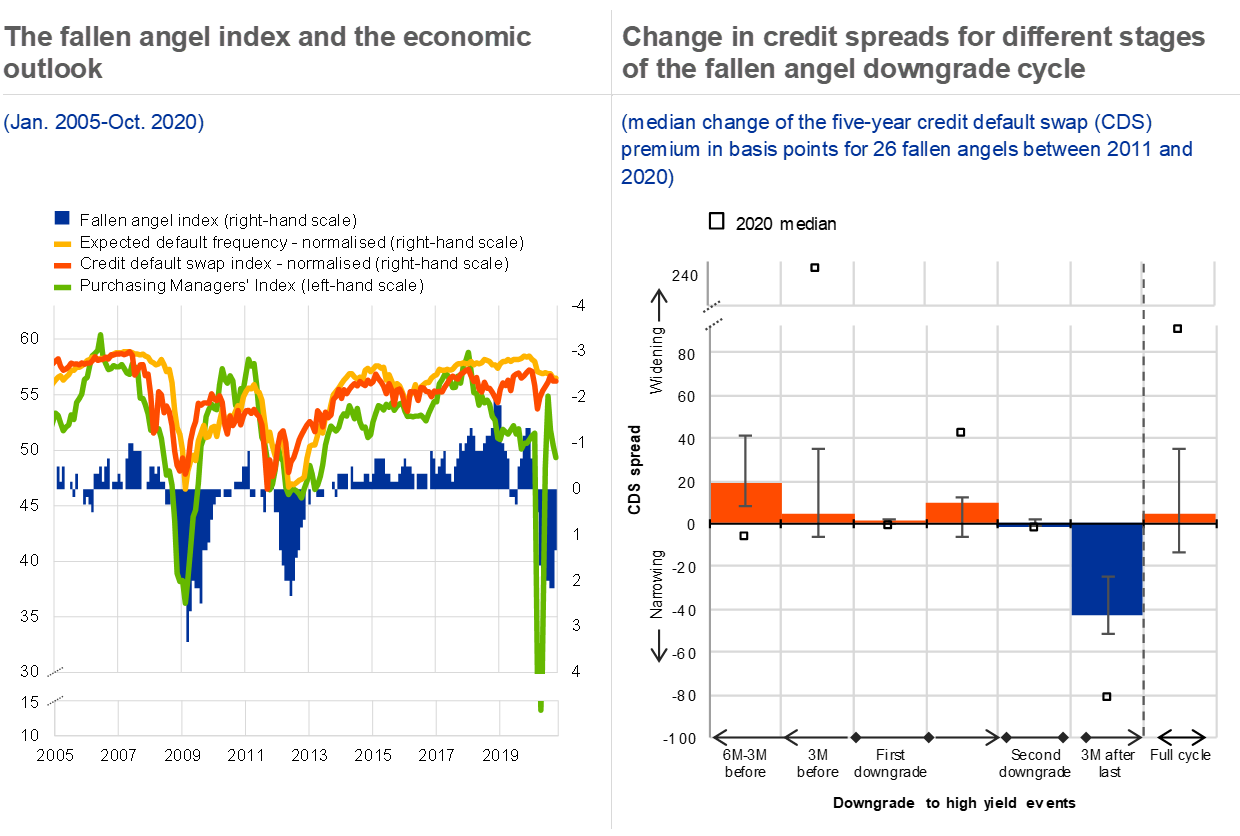

Chart A

Downgrades reflect the economic outlook and risk perceptions, while markets are forward-looking

Sources: Fitch Ratings, Moody’s Analytics, S&P Global Market Intelligence, Bloomberg Finance L.P., IHS Markit, Credit Market Analysis and ECB calculations.

Notes: Left panel: the right-hand scale is inverted. The fallen angel index is calculated as the number of downgrades from investment grade to high yield minus the number of upgrades from high yield to investment grade, expressed as a six-month moving average. The expected default frequency (EDF) is a 12-month-ahead EDF from Moody’s. Both the EDF and the credit default swap index (iTraxx Europe main index) have been normalised and rescaled for visualisation purposes. Right panel: the chart shows the change in the five-year CDS premium over various stages of the credit deterioration process for a sample of 26 fallen angels (euro area non-financial corporations with quoted contracts). The error bars indicate the 40th and 60th percentiles of the distribution. The change on the downgrade date is measured as the difference between the level on the announcement date and the level on the day before. The change in the CDS premium is adjusted for changes in the iTraxx Europe main index, following Hull, J., Predescu, M. and White, A., “The relationship between credit default swap spreads, bond yields, and credit rating announcements”, Journal of Banking and Finance, Volume 28, Issue 11, 2004, pp. 2789-2811.

Credit deterioration and market repricing do not happen instantaneously after a downgrade, occurring instead over an extended period which typically precedes the actual downgrade. Although credit rating downgrades always depend on company-specific factors, there is also a relationship with expectations for economic activity. Generally, CRA decisions for fallen angels have followed the main turning points in the Purchasing Managers’ Index, including the current downturn stemming from the coronavirus pandemic (see Chart A, left panel). Changes in credit risk perceptions typically precede an issuer’s downgrade, including when CRAs do not place an issuer on a negative outlook or watch list. CDS premia generally widen before a company is first downgraded to below investment grade by one of the CRAs, followed by only a small market reaction immediately afterwards. A partial recovery is seen after an issuer loses its last investment-grade rating (see Chart A, right panel), suggesting that a fallen angel’s securities are undervalued at this point. Fallen angels since February 2020 follow this pattern, but with a swifter and stronger increase in the credit premium before the first downgrade, as seen most notably in the severely affected airline industry. This analysis is, however, based on historical data, and may not be representative of extreme systemic scenarios with many concurrent downgrades.

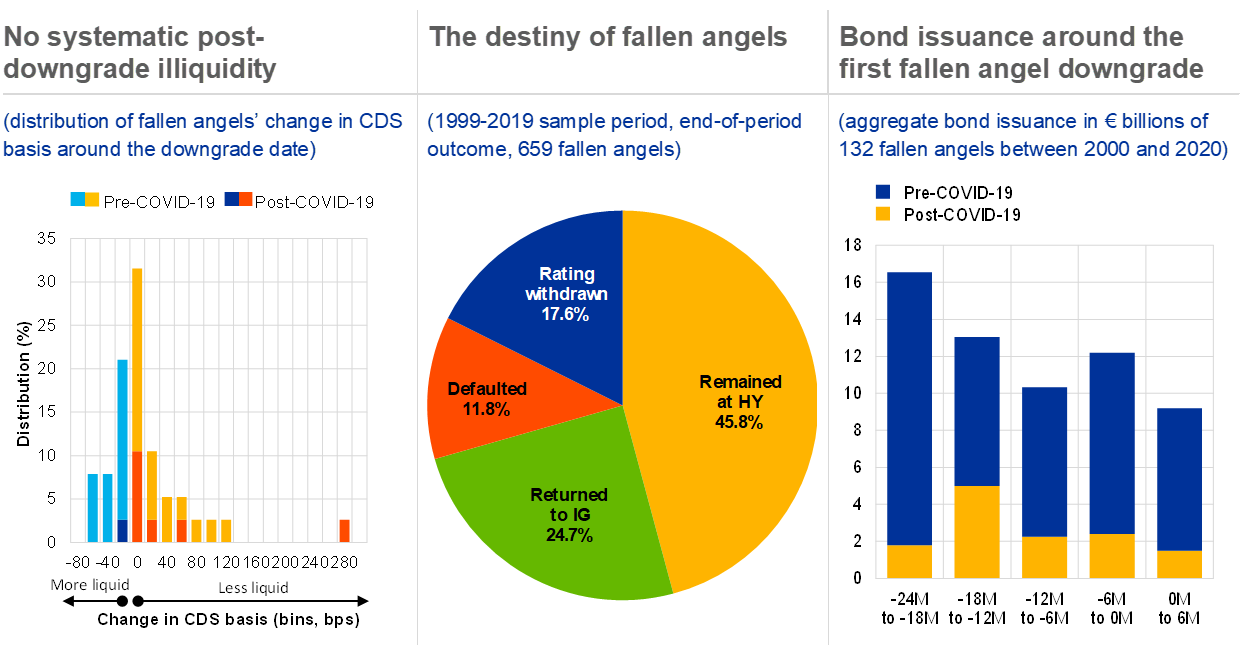

In general, fallen angel downgrades have not led to abnormal or sudden post-event illiquidity, but there have been some notable responses during the coronavirus turmoil. Bond yields can increase after a downgrade if the market for these securities becomes less liquid. An indicator of a security’s liquidity, the CDS basis, does not show broad evidence of abnormal post-downgrade illiquidity (see Chart B, left panel).[2] Nevertheless, pandemic-related downgrades show some post-event illiquidity, which may be explained by the relatively sudden change in the broader economic outlook and wider market stress.

The impact of forced sales is softened by differences in the definition of “investment grade” and flexibility in investment funds’ mandates. Empirical evidence shows that a security’s weight in funds’ portfolios is reduced around the time of a fallen angel downgrade, whereas this is not seen for other downgrades. However, the definition of “investment grade” varies across index providers, which means that an issuer can be categorised as investment grade by some and high yield by others.[3] In addition, passive bond funds linked to indices do not always replicate an index in full, with 93% of funds using some form of optimised sampling. Funds also have some flexibility to retain a security for some time after it is removed from the index, meaning that sales can be spread out over time.[4]

The fate of a fallen angel is not sealed, yet fallen angels do face more challenging issuance conditions. According to Moody’s data over a 20-year period, nearly a quarter of fallen angels returned to investment grade, almost half remained in the high-yield category and 12% defaulted (see Chart B, middle panel). But a downgrade to below investment grade is associated with lower bond issuance volumes (see Chart B, right panel). Market intelligence suggests that firms frontload bond issuances when a downgrade to below investment grade is impending. In other cases, an increase in a firm’s debt issuance may have led to downgrades in the first place.

The widening of credit spreads ahead of fallen angel downgrades gives some indication of the risks posed by large-scale downgrade scenarios. If a larger cohort of firms were to face such pressures on their cost of funding, this would increase their vulnerability to shocks in the near term and could weigh on their investment in the longer term, creating wider macroeconomic costs.[5] That said, past episodes also give some comfort that the systemic impact of forced sales may be contained if they are spread out over time and/or can be anticipated. This does not imply that forced sales do not occur; rather, it means that their impact is cushioned outside of large, systemic scenarios.

Chart B

A fallen angel’s bond issuance declines, but its fate is not sealed

Sources: Bloomberg Finance L.P., Dealogic, Credit Market Analysis, Moody’s Analytics and ECB calculations.

Notes: “Pre-COVID-19” refers to events before February 2020. Middle panel: sample includes 659 companies. Ratings are withdrawn when a firm is acquired, for example. HY: high yield; IG: investment grade.

- See, for example, “A system-wide scenario analysis of large-scale corporate bond downgrades”, ESRB technical note, July 2020.

- The CDS basis is the spread between the option-adjusted Z-spread (a security’s spread over the zero-coupon government bond yield reference curve) and the CDS spread of a similar maturity.

- Most bond indices consider issue ratings from the three largest CRAs. Index providers use rating rules such as: average, median, or minimum out of three.

- See, for example, page 31 of the iShares III Public Limited Company Prospectus: “[…] issues may be downgraded […]. In such event the Fund may hold non-investment grade issues until such time as the non-investment grade issues cease to form part of the Fund’s Benchmark Index (where applicable) and it is possible and practicable (in the Investment Manager’s view) to liquidate the position.”

- See also Kalemli-Özcan, S., Laeven, L. and Moreno, D., “Debt overhang, rollover risk, and corporate investment: evidence from the European crisis”, Working Paper Series, No 2241, ECB, February 2019.