Euro area equity markets and shifting expectations for an economic recovery

Published as part of the ECB Economic Bulletin, Issue 5/2020.

Recent developments in equity prices and earnings growth expectations

As a result of the expected economic fallout from the global spread of the coronavirus (COVID-19) and the considerable associated uncertainty, euro area equity prices fell by more than 30% from February to mid-March 2020 (see Chart A). At the same time, liquidity conditions worsened significantly, as reflected in a pronounced widening of bid-ask spreads – a development which was not confined to equity markets.

Chart A

Euro area and US equity prices

(1 January 2019 = 100)

Sources: Refinitiv and ECB calculations.

Notes: The euro area index refers to the broad Dow Jones Euro Stoxx and the US index refers to the S&P 500. The vertical lines denote (from left to right) the Friday before the onset of coronavirus-related financial market turmoil (21 February 2020) and the PEPP announcement (18 March 2020). The latest observation is for 14 July 2020.

With the announcement of the pandemic emergency purchase programme (PEPP), euro area equity prices started to recover (see Chart A) and market functioning has moved closer to normal levels, with bid-ask spreads decreasing sharply. Equity prices, especially those of US non-financial corporations (NFCs), also improved considerably, buoyed by the measures taken by central banks and governments in many countries. The recovery in equity prices looks even stronger when judged against the historical distribution of forward-looking valuation metrics (see Chart B). Owing to adjustments in near‑term earnings expectations and a near normalisation in equity risk premia, forward price‑earnings ratios (P/E ratios) for NFCs have now moved above pre-COVID-19 levels. While this is also the case for euro area banks, their valuations remain more subdued. However, in the light of the recent rapid adjustments in earnings expectations, the information value of price‑earnings measures should be taken with caution.

Chart B

Accounting-based equity valuation metrics

(distributions since 1987) Sources: Refinitiv and ECB calculations.

Notes: The forward-looking P/E ratio for the euro area has been recorded monthly since 1987. The latest observation is for 14 July 2020.

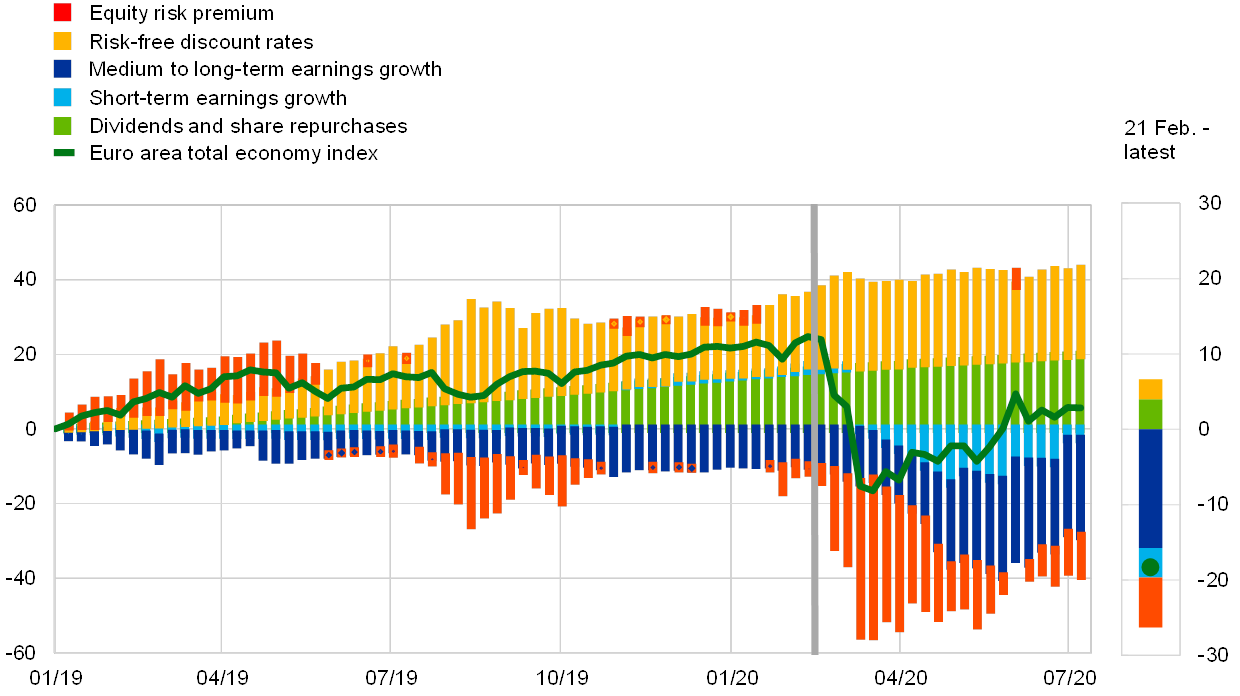

The main reason for the rebound in equity prices is a recovery in risk sentiment which, based on a decomposition using a dividend discount model, seems to have more than compensated for the declines in earnings expectations (see Chart C). Between early February and mid-March 2020 the euro area equity risk premium (ERP) increased from 8% to 12%, before decreasing to below 9% after the PEPP announcement. Although there is some uncertainty surrounding the estimation of the ERP, according to a dividend discount model, the fluctuations in the ERP explain both the lion’s share of the initial decline in equity prices and most of the subsequent recovery. At the same time, analysts’ earnings expectations have been adjusted downwards. In the wake of the lockdown measures implemented across euro area countries, shorter-term earnings growth expectations turned negative for the first time since 2009, but they appear to have troughed recently as the economic recovery is expected to gradually take hold. By contrast, until mid-April 2020 analysts’ longer-term earnings expectations remained surprisingly resilient, in line with prospects of a strong and rapid recovery in earnings (see Chart D). More recently, they have been adjusted downwards by more than 3 percentage points to below 8% per annum. Despite this drop, longer-term earnings expectations remain higher than at the low point of the global financial crisis.

Chart C

Dividend discount model decomposition of euro area equity prices and Euro Stoxx earnings growth expectations

(left-hand scale: percentages, cumulative change re-based to zero in January 2019; right-hand scale: percentages, cumulative change since 21 February 2020)

Sources: Refinitiv, IBES, Consensus Economics and ECB calculations.

Notes: The decomposition is based on a dividend discount model. The model includes share buybacks, discounts future cash-flows with interest rates of appropriate maturity and includes five expected dividend growth horizons. For more details, see the article entitled “Measuring and interpreting the cost of equity in the euro area”, Economic Bulletin, Issue 4, ECB, 2018. The vertical line denotes the Friday before the onset of coronavirus-related financial market turmoil (21 February 2020). The latest observation is for 10 July 2020.

Chart D

Euro Stoxx earnings growth expectations

(percentages per annum)

Sources: Refinitiv, IBES and ECB calculations.

Notes: Total market-expected earnings growth is over horizons of 12 months and three to five years. The vertical line denotes the Friday before the onset of coronavirus-related financial market turmoil (21 February 2020).The latest observation is for 10 July 2020.

Equity prices and short versus longer-term revisions to the macro outlook

In the light of the ongoing gradual downward adjustment of longer-term earnings prospects, the recovery in short-term earnings prospects has been an important counterbalance. Equity prices reflect the discounted value of all future dividend streams, where the weight of dividends in the near term depends on the investor’s discount factor (including the required ERP). Therefore, the (initial) resilience of longer-term earnings prospects (more than one year ahead) and the recent recovery in short-term earnings prospects (i.e. over the next year) could explain some of the relative robustness of and recent recovery in equity prices. Results of a regression analysis which makes use of past Consensus Economics forecast vintages to assess the impact of past changes in GDP growth expectations on equity prices at different horizons suggest that investors tend to attach equal weight to short-term forecasts and longer-term expectations when evaluating the market implications of macroeconomic developments. Overall, the risk of significant further declines in equity prices still remains, especially if long-term GDP growth expectations are adjusted down further or the recent upward revisions to the near‑term outlook decline again (as a result of a potential second wave of the coronavirus and consequent policy responses, for example).

Signals about the shape of the recovery derived from earnings per share forecasts, dividends and options

In addition to analysts’ longer-term earnings growth expectations, earnings per share (EPS) forecasts also continue to be revised down at longer horizons (see Chart E). In mid-March 2020 the pattern of surveyed quarterly earnings forecasts continued to largely signal a V-shaped recovery, despite weak realised earnings in the first quarter of 2020. Analysts foresaw a rapid recovery from the second quarter onwards as economies were expected to gradually emerge from lockdown. Since then, notwithstanding the announcement of the PEPP, the general level of medium-term earnings expectations has continued to be revised downwards, even though euro area stock prices recovered over the same period.

Chart E

Euro Stoxx EPS forecast

(EUR per share)

Sources: Refinitiv, IBES and ECB calculations.

Notes: Market capitalisation weighted aggregate of individual firms’ EPS and EPS forecasts (weekly data). 12 March 2020 is the date of the March 2020 Governing Council meeting. The latest observation is for 14 July 2020.

The assessment of the future outlook appears even less sanguine when judged on the basis of futures pricing rather than surveys (see panel (a) of Chart F). The term structure of claims on future dividend payments, known as dividend strips, shows that markets expect dividends to lie far below pre-COVID-19 levels in the near future. Although dividend futures prices with maturities of more than two years are slightly higher than before the PEPP announcement, they remain well below the prices observed prior to the global spread of COVID-19.

Chart F

Euro Stoxx 50 dividend strips and term structure of the euro area equity risk premium calculated from options prices

(panel (a): EUR; panel (b): percent)

Sources: Refinitiv, IBES and ECB calculations.

Notes: Panel (b) shows the term structure of the ERP estimated following I. Martin, “What is the Expected Return on the Market?”, The Quarterly Journal of Economics, Vol. 132, No 1, 2017, pp. 367-433. The latest observation is for 14 July 2020.

In addition, risks of renewed price corrections in the near future continue to be seen as likely, as indicated by the term structure of the equity risk premium (see panel (b) of Chart F). Estimating the ERP from options prices at horizons between 1 and 24 months shows that the term structure of the ERP is likely to be upward sloping during normal times, as was (marginally) the case in February 2020, for instance, and downward sloping in times of financial stress, caused by the risk of large potential losses in the near future. In line with this conjecture, and immediately before the announcement of the PEPP, the ERP at the one-month horizon surged to around 30%. Despite a significant decline since then, the ERP still remains well above the levels seen in February at all horizons and the term structure slope continues to be inverted.

Other option-based measures of uncertainty also continue to stand at heightened levels and left tail risk remains very elevated (see Chart G). The risk-neutral distribution of expected returns by investors can be extracted from options prices.[1] Since options contracts with different maturities are traded at any point in time, it is possible to derive a term structure of the investors’ risk-neutral distribution of expected returns. Between February and late March 2020 there was a substantial reduction of left tail risk (“bad risk”) relative to right tail risk (“good risk”), as implied by the reduction in the skewness coefficient of the Euro Stoxx 50 risk‑neutral density derived from options prices (see left-hand panel of Chart G).[2] Already in early February, before the outbreak of the COVID-19 pandemic in Europe, options markets signalled a large imbalance of left tail risk two to three months ahead, with a reduction afterwards. Following the equity market correction, the implied left tail risk and right tail risk became more balanced for the months ahead. This was the result of investors starting to attach more weight to the possibility of a further price recovery (i.e. increasing the odds of good risk versus bad risk) and was in line with a decline in the ERP since the height of the pandemic. However, owing to the recent cascade of negative economic news and fears of a new virus wave, the risk-neutral distribution remained highly skewed to the left when compared with historical episodes (see right-hand panel of Chart G). Moreover, uncertainty as indicated by the variance of the distributions is still elevated.

Chart G

Pearson skewness coefficient of the Euro Stoxx 50 risk-neutral density

(coefficient)

Sources: Bloomberg and ECB calculations.

Notes: The dates in the left-hand panel have been chosen to give an overview of the pandemic period. The blue shaded area in the right-hand panel denotes the range of the Pearson skewness coefficient over the period from October 2008 to January 2009. The latest observation is for 9 July 2020.

- It is important to keep in mind that risk-neutral measures embed investor’s risk attitudes. Changes in the risk-neutral distribution can be the result of changes in the expected quantity of risk or changes in the investors’ risk aversion (price of risk). For more details, see the box entitled “Coronavirus (COVID‑19): market fear as implied by options prices”, Economic Bulletin, Issue 4, ECB, 2020.

- The Pearson skewness coefficient of the Euro Stoxx 50 risk-neutral density derived from options prices compares the extent of left tail risk (“bad risk”) relative to right tail risk (“good risk”). This index is below zero if left tail risks outweigh right tail risks.