Macroprudential capital buffers – objectives and usability

This article discusses the capital buffer framework under Basel III, with particular focus on the issue of buffer usability. Capital buffers are a key element of the regulatory framework, inter alia aimed at enabling banks to absorb losses while maintaining the provision of key services to the economy. Although buffers are intended to be used in a crisis, anecdotal evidence suggests that banks can be unwilling to draw them down as needed, with potentially adverse effects for the economy. The article emphasises the importance of clear and convincing communication for mitigating a number of impediments to buffer usability. It also calls for a medium-term rebalancing between structural and cyclical capital requirements, as a greater share of capital buffers that can be released in a crisis would enhance macroprudential authorities’ ability to act countercyclically.

1 Objectives of the capital buffer framework

The capital buffer framework for banks is one of the main new elements of the Basel III regulatory framework. Introduced after the global financial crisis of 2007‑09, Basel III addresses a number of shortcomings in the pre-crisis regulatory framework and provides a foundation for a resilient banking system that is able to support the real economy through the economic cycle (see BCBS, 2011). Capital buffers play an important role in this respect, as they are inter alia meant to mitigate procyclicality by acting as shock absorbers in times of stress. In the European framework, these buffers include the capital conservation buffer (CCoB), the countercyclical capital buffer (CCyB), buffers for global and other systemically important institutions (G-SIIs and O-SIIs) and the systemic risk buffer (SyRB). The combination of all these buffers constitutes the combined buffer requirement (CBR).

Capital buffers aim to enable banks to absorb losses while maintaining the provision of key services to the real economy, while automatic restrictions on distributions prevent the imprudent depletion of capital in times of stress. Buffers are placed on top of minimum capital requirements to enhance banks’ resilience against shocks. They provide banks with space to absorb losses as they are incurred. At the same time, by enabling banks to maintain the provision of key financial services to the real economy without breaching minimum capital requirements, buffers mitigate negative externalities related to excessive deleveraging or fire sales that could otherwise harm the economy. Moreover, when operating below the CBR, banks face automatic restrictions on distributions, including dividends, bonus payments, and coupon payments on Additional Tier 1 (AT1) instruments. The purpose of these restrictions is to prevent the depletion of capital during a stress episode, such as observed during the global financial crisis, and to replenish the buffers instead.[2]

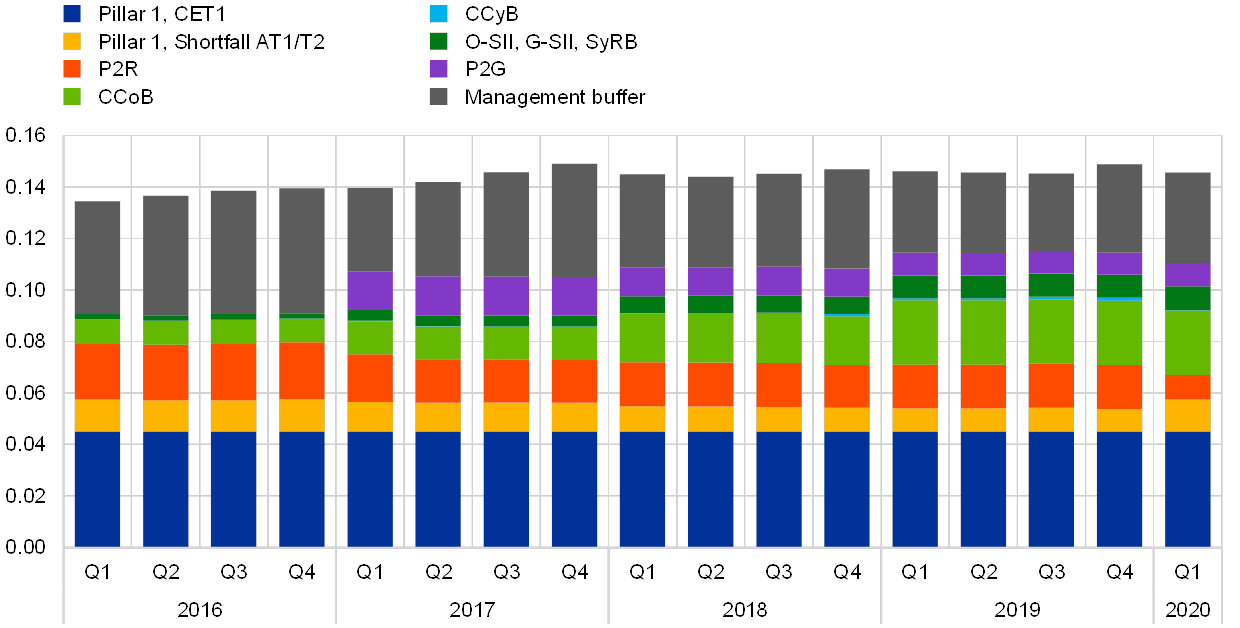

In recent years, banks in the euro area have increased their capital ratios considerably and built up capital buffers, in line with the timelines provided for in the framework. The Common Equity Tier 1 (CET1) capital ratio increased from 13.4% in 2016 to 14.6% in the first quarter of 2020 (see Chart 1). Starting in 2016, capital buffer requirements, such as the CCoB (in light green) and the buffers for G-SIIs and O-SIIs and the SyRB (in dark green), were phased in, increasing the total amount of required capital. Moreover, banks hold significant management buffers over and above current capital requirements. Notably, while the European banking sector has built up significant capital buffers since the global financial crisis, the role played by the CCyB has been limited, as it was set at 0% in many euro area countries at the onset of the coronavirus (COVID-19) pandemic.

Chart 1

Evolution of bank capital ratios and their components in the euro area

(percentages of risk-weighted assets)

Sources: ECB supervisory statistics and ECB calculations.

Note: Based on requirements and CET1 capital ratios of a sample of around 500 significant and less significant institutions reported at the highest level of consolidation. The reduction in P2R observed for 2020 is due to a change in the composition of capital that can be used to fulfil these requirements.

2 Possible trade-offs between the objectives of the buffer framework

While the various elements of the capital buffer framework are generally complementary, trade-offs and conflicts between them may exist in times of systemic stress. Over the medium term, the buffer framework aims to ensure a sound and stable banking system that is able to continuously provide key services to the economy. The various elements of the framework complement each other in achieving this ultimate objective; they make sure that banks build up a sufficient amount of capital to flexibly absorb shocks, and they prevent the imprudent depletion of capital resources by imposing distribution restrictions during stress episodes. Following the materialisation of a systemic shock, however, when a number of banks may have to use the buffers as envisaged by the framework, conflicts between the objectives of the framework could arise.

Maintaining lending at the onset of a crisis may help to reduce the amount of capital that will be needed to absorb losses further down the road. At least initially, avoiding deleveraging or even expanding the balance sheet in response to a shock reduces the capital buffer that is available in the banking system to absorb losses throughout the subsequent crisis. This suggests a possible trade-off between the buffer framework’s different objectives, since the ability to absorb losses may be lower in a situation where banks keep lending after a shock, at least in the near to medium term, which could increase the risk of an individual bank failure and the likelihood of a banking crisis. However, if the banking sector in aggregate maintains or expands the supply of loans at the onset of a crisis, this may help to alleviate the downturn and decrease losses later on in the crisis. Thus, fewer losses would have to be absorbed in total, which mitigates the possible trade-off between the two objectives (see the article entitled “Buffer use and lending impact” in this issue of the Macroprudential Bulletin for a quantitative simulation of this effect). Importantly, for this benefit to materialise, it is necessary that the banking system collectively takes this positive externality into account in its lending behaviour. This may not necessarily be the case, as collective action problems may prevent individual banks from factoring the social benefits of the continued provision of key economic services into their private lending decisions.

While automatic constraints on distributions following a breach of the CBR help to prevent imprudent depletion of capital, they may also induce banks to take undesirable adjustment actions in order to avoid being constrained. Constraints on distributions after a breach of the CBR help to maintain resilience by preserving capital, and can thereby strengthen the ability to support lending. They address one of the problems observed during the global financial crisis, in which some banks continued to make distributions while already anticipating future losses. However, distribution constraints may also undermine banks’ willingness to operate below the CBR and could therefore trigger undesirable adjustment actions (such as deleveraging or shifts towards less risky assets), which would then negatively affect lending. Thus there could be a trade-off between the buffer framework’s objective of maintaining the provision of key services and the objective of preventing the imprudent depletion of capital that is associated with the mechanism for automatic restrictions on distributions.

3 The concept of buffer usability

For buffers to fulfil their role as shock absorbers, it is essential that banks are willing to make use of them in times of systemic stress, so that excessive deleveraging and the exacerbation of the initial downturn can be avoided. Avoiding excessive deleveraging by the banking sector in a downturn is important owing to the relevance of aggregate bank balance sheet size for the future path of the economy. As evidenced by the crisis of 2007-09, a shortfall in credit supply (a “credit crunch”) can have material negative effects on GDP growth. Similarly, the economy may be negatively affected if banks withdraw from other activities that are economically relevant (e.g. market making, ownership of central counterparties, lending to other banks).

Excessive deleveraging may occur in situations where banks want to avoid or mitigate deteriorations in their capital ratios, and usable capital buffers can help to prevent such undesirable behaviour. Stress episodes usually imply losses for banks, leading to declines in capital ratios. Banks can mitigate such effects by reducing the size of their balance sheet, i.e. by engaging in deleveraging action, or by shifting their portfolio towards safer borrowers and crowding out riskier (often smaller) borrowers. As noted above, such deleveraging can be harmful for the economy if it becomes excessive, which is why the buffer framework aims to ease the pressure to adjust. Specifically, the CCyB can be released in a downturn, which reduces the threshold at which banks are subjected to automatic restrictions on distributions. In addition, banks are explicitly allowed to operate below the remaining capital buffer requirements when needed, subject to automatic restrictions on distributions. In other words, it is the intention of the framework that banks should use the buffers in a stress episode, so that excessive deleveraging can be avoided.

Buffers are considered usable if banks are willing to operate within the CBR, while avoiding undesirable adjustment actions such as excessive deleveraging. Capital ratios may decline and eventually fall below the CBR for various reasons. First, the materialisation of losses reduces the amount of capital that is available to the bank, i.e. the numerator of the capital ratio. Moreover, risk weights tend to increase in stress periods and bank assets may expand as firms draw on committed credit lines, thereby raising the amount of risk-weighted assets, i.e. the denominator of the capital ratio.[3] Banks’ capital ratios may therefore fall below the CBR when a sufficiently large amount of capital has been wiped out and/or when there has been a substantial increase in risk weights for the existing portfolio (this can be described as “passive” use of the buffers). Second, an expansion of the balance sheet (e.g. an increase in the amount of loans) or an increase in the share of assets with higher risk weights in the portfolio will also increase the amount of risk-weighted assets. Again, capital ratios may fall below the CBR if the balance sheet or the share of risky exposures is expanded by a sufficient amount (this can be described as “active” use of the buffers).[4] In both of these cases, buffers are considered usable if banks do not take undesirable adjustment actions (such as excessive deleveraging) to avoid a breach of the buffer requirements or to shorten its duration.

4 Possible impediments to buffer usability

Although buffers are intended to be used as defined above, there are a number of factors that may undermine banks’ willingness to accept a decline in capital ratios, including market factors, supervisory and macroprudential factors, and regulatory factors. Many of these factors relate to some form of stigma, attached either to a breach of the CBR (potentially further strengthened by the associated restrictions on distributions) or to operating with capital ratios below market expectations. This concern may become more relevant in a systemic crisis, during which banks want to avoid being the first to be stigmatised, and hence may engage in undesirable adjustment actions that may seem individually rational but can be collectively damaging (such as excessive deleveraging). Collective action problems may arise if individual banks fail to properly consider the social benefit of stabilising the economy and the banking sector through the use of the buffers. Uncertainty over the future path of the crisis or existing vulnerabilities in the sector could also play a role. In addition to the issue of stigma, which is about perception, there could also be difficulties relating to constraints stemming from other regulatory requirements and supervisory tolerance of buffer use.

Market-based factors that may undermine the usability of capital buffers include the following:

- Higher funding costs: Banks’ funding costs could increase or the availability of funding could become restricted once capital ratios start to decline (owing to the increase in perceived default risk). This effect may be exacerbated by the potential stigma when a breach of the CBR becomes public knowledge. It could also be further aggravated if the decline in capital ratios is associated with an expansion in lending, as, in times of crisis, the latter may be associated with excessive risk-taking.

- Possible rating downgrades: Banks’ capital positions are an important factor in their credit rating, which affects banks’ access to and cost of funding as well as their reputation more broadly.[5] As for the funding cost factor, rating downgrades may occur either because of the negative signal associated with a breach of the CBR or because of the decline in capital ratios (and the increase in default risk) more generally.

Regulatory and prudential factors include the following:

- Distribution restrictions: Banks would face automatic restrictions on distributions when operating below the CBR. These restrictions on dividend, bonus and AT1 coupon payments would have negative effects on investors and bank executives. To maintain a strong relationship with investors, and also to avoid triggering the market factors outlined above, banks may prefer to deleverage rather than face automatic restrictions. Concerns about distribution restrictions may be particularly relevant for certain instruments, such as AT1 bonds, since market intelligence suggests that a cancellation of a coupon payment could be seen as a particularly adverse signal – even if coupon payments are contractually set to be discretionary.

- Existence of other regulatory/prudential requirements: Other regulatory and prudential requirements – such as the leverage ratio or the minimum requirement for own funds and eligible liabilities – may reduce the usability of the CBR if they become more binding than the risk-based requirement. The use of buffers may also be curtailed if banks wish to maintain a sufficient margin above the regulatory minimum requirement within the risk-based framework (i.e. the sum of Pillar 1 and Pillar 2 minimum requirements).

- Concern and uncertainty about prudential authorities’ follow-up and their willingness to tolerate buffer use: Banks might want to avoid the increased supervisory scrutiny associated with a breach of the CBR, and such scrutiny is likely to increase the closer the bank comes to the minimum requirement, raising concerns regarding its viability. In addition, banks may face uncertainty with respect to the time they would have to restore their capital buffers after the initial breach of the CBR, unless this is clearly communicated by the supervisor. Finally, banks may be concerned about the speed of capital buffer increases once the crisis is over and conditions normalise. Such concerns may be more relevant at times when profitability is low or access to capital markets is constrained.

All of the factors mentioned above can induce banks to set capital ratio targets in order to optimise funding costs while minimising the risk of default, rating downgrades and supervisory or regulatory intervention. Prudential and regulatory factors are one determinant of these target ratios, as banks may want to allow for sufficient (varying or constant) management buffers above the threshold of regulatory intervention. But other factors, such as market pressure or the possibility of a rating downgrade, may also affect these target ratios and might become more relevant in a crisis situation (e.g. market pressure to maintain higher capital ratios might become more pronounced in a situation where macroeconomic uncertainty increases, and this could lead to capital ratio targets becoming decoupled from the CBR – see the article entitled “Financial market pressure as an impediment to the usability of regulatory capital buffers” in this issue of the Macroprudential Bulletin).

5 Policy implications of the COVID-19 crisis

Initial policy reaction in response to the crisis

European and national authorities took swift measures to address the impact on the financial sector of the coronavirus pandemic. Several euro area macroprudential authorities (including central banks and banking supervisors) reduced macroprudential buffer requirements, releasing more than €20 billion of CET1 capital held by euro area banks.[6] Specifically, in several of the countries where the CCyB was positive or was in the course of being activated, authorities reduced the requirement or halted its activation. In other countries increases were revoked. In some countries, the SyRB was also fully released or lowered, while buffers on selected O-SIIs were reduced. In addition, some countries revoked or delayed the entry into force of previously announced measures, such as buffers on O-SIIs or the introduction of capital surcharges on domestic mortgage loan exposures under Article 458 of the Capital Requirements Regulation (CRR).

The macroprudential measures complemented action taken by ECB Banking Supervision. Starting on 12 March 2020, ECB Banking Supervision announced a number of temporary capital and operational relief measures in response to the COVID-19 shock. Banks were allowed to operate below Pillar 2 guidance (P2G) and the composition of Pillar 2 requirements (P2R) was changed to include AT1 or Tier 2 (T2) instruments, bringing forward a change that was initially scheduled to come into effect in January 2021.[7] These supervisory measures freed up €120 billion of CET1 capital. In order to retain capital in the banking system, ECB Banking Supervision also recommended banks not to pay dividends for 2019 and 2020 and to refrain from buying back shares at least until December 2020. In addition, banks were encouraged to avoid excessive procyclical effects when applying International Financial Reporting Standard (IFRS) 9.

The above measures provided significant capital relief aimed at enabling banks to continue fulfilling their role in funding the real economy as the economic effects of the COVID-19 shock became apparent. As a result of the measures, management buffers increased by 1.5 percentage points for euro area banks and currently stand at 4.9% of risk-weighted assets, as measured on the basis of euro area banks’ balance sheets in the fourth quarter of 2019. This relief strengthened banks’ capacity to absorb potential future losses related to the repercussions from the coronavirus while avoiding undesirable adjustment actions, such as excessive deleveraging. The measures were complemented by a number of public statements – including from ECB Banking Supervision, the Basel Committee on Banking Supervision (BCBS), and the Financial Stability Board (FSB) – confirming that the use of the Basel III capital buffers to absorb losses and support lending in these times of crisis is consistent with a well-functioning, prudently managed banking system and with the design and intended functioning of the Basel III framework.[8]

Reflections on the way forward

Clear and convincing communication can help overcome supervisory impediments to buffer usability and, possibly, also market-based impediments. In their communications, prudential authorities have repeatedly stated that using buffers today would be in line with the expectations set out in the regulatory framework. This message clarifies authorities’ expectations and can help overcome impediments to buffer usability stemming from uncertainty about supervisory follow-up action. Moreover, clear and credible communication on the use of buffers also helps inform the expectations of financial market participants, thereby limiting the possible stigma associated with banks’ use of buffers.

Shaping agents’ expectations on the path towards replenishing used buffers will also help to enhance their usability. In the euro area, ECB Banking Supervision has already committed to allowing banks to operate below P2G and the CBR until at least the end of 2022, and clarified that it will not require banks to start replenishing their capital buffers before the peak in capital depletion is reached.[9] Moreover, it is taking steps to develop a well-designed and credible path to normality, further addressing banks’ uncertainty over the expected speed of buffer replenishment and thereby enabling them to factor the release into their capital planning. The path to normality will take into account evidence on the severity of the shock, bank-specific circumstances, and the need to preserve the sector’s fundamental role in lending to the real economy during the recovery.[10] Despite the many complexities and uncertainties, communication on the time that banks will be given to rebuild buffers during the recovery, as well as on the factors that would steer such decisions, brings additional benefits by enhancing banks’ willingness to make use of the buffers.

Beyond communication shaping banks’ expectations and encouraging them to make use of the buffers in case of need, close monitoring is necessary to assess the need for further possible policy interventions in the short to medium term. The issue of buffer usability needs to be closely monitored, as it is still uncertain whether banks would be willing to make use of the buffers in case of need. Depending on the type of potential impediment, further targeted or broad-based policy measures could become necessary if and when losses start to materialise or if new lockdowns are needed, adding further uncertainty to the recovery. Such policy measures would become particularly relevant if there are any signs of potential credit supply constraints caused by the design of the buffer framework that could deepen the recession.

Implications for future policy design

Releasable buffers can help to mitigate the possible impediments to buffer usability described above. While clear evidence is not yet available, the discussion summarised in this article and the initial evidence presented in the article entitled “Financial market pressure as an impediment to the usability of regulatory capital buffers” in this issue of the Macroprudential Bulletin suggest that, even in a stress situation, banks might be reluctant to operate with capital ratios below the CBR. A possible way to address this issue would be to enhance the role of releasable capital buffers within the capital framework. Following the release of a specific buffer requirement, banks can operate with lower capital ratios without breaching the CBR and without being subject to automatic restrictions on distributions. This should help to address several of the impediments to buffer usability mentioned in Section 4 and thereby enhance banks’ ability to absorb losses while maintaining the provision of key economic services during a stress episode.

The limited availability of releasable capital buffers in the COVID-19 crisis constrained macroprudential authorities’ ability to act countercyclically. As illustrated in Chart 1, the share of releasable macroprudential capital buffers has been limited during the current crisis, as in the build-up phase of capital requirements countercyclical instruments were crowded out by structural elements of the capital stack. Among the existing macroprudential buffers, only the CCyB is designed to be released in a downturn, but in the euro area the CCyB amounted to only 0.1% of risk-weighted assets at the onset of the pandemic. Other buffers, like the SRyB or the O-SII buffer, have a more structural nature. Although a release of such buffers is possible in principle, in many cases this would not be in line with the original objectives of their activation or with their operational frameworks. Moreover, unless accompanied by clear communication, the release of structural buffers could impair the credibility of the macroprudential framework and generate uncertainty over the future application of the buffers.

The need to enhance authorities’ ability to act countercyclically calls for a rebalancing between structural and cyclical elements of the capital stack. For example, the creation of a positive rate for the CCyB in normal times would be a move in this direction and enhance the ability of macroprudential authorities to address unforeseen events, such as the COVID-19 pandemic. Taking into account the experience gained during the coronavirus pandemic, a thorough review of the buffer framework is warranted to assess how a rebalancing between structural and cyclical buffers in the capital stack can best be achieved.

Any adjustments to the framework would have to ensure that all of the buffer framework’s current objectives continue to be met. For this reason, a clear framework for the timely restoration of releasable elements in the capital stack would be needed. In the case of Europe and the Banking Union in particular, a strong coordination mechanism at the European level is warranted to ensure consistent application of the release and the build-up of buffers across countries.

6 Conclusion

This article outlines the main objectives of the capital buffer framework introduced with Basel III and reviews the possible trade-offs that may arise between these objectives. It explains the concept of buffer usability and examines a number of impediments that may limit the use of buffers. Buffers are considered usable if banks are willing to operate with capital ratios below the CBR while avoiding undesirable adjustment actions such as excessive deleveraging. Regulatory, prudential and market-based impediments may, however, limit banks’ willingness to use available buffers and allow capital ratios to decline.

To ensure that the prudential policy measures already implemented remain appropriate, the issue of buffer usability needs continuous monitoring. This represents one of the main policy challenges over the coming months, as a strong economic recovery essentially requires banks to be willing to use their regulatory capital buffers (see the article entitled “Buffer use and lending impact” in this issue of the Macroprudential Bulletin for further discussion on this). Beyond immediate reactions of market participants and banks to a potential use of the buffers, authorities need to monitor whether a possible reluctance by banks has an impact on lending to the real economy as a result of undesirable actions, such as excessive deleveraging or de-risking.

Further policy measures may become necessary if market and regulatory impediments lead to undesirable adjustments; in the medium-term, a rebalancing between the structural and cyclical elements of the capital stack would be welcome. While prudential authorities were swift to react to the crisis, further policy measures may still be needed to ensure that existing buffers are usable as envisaged by the framework. Moreover, a better balance between structural and cyclical elements of the capital stack would increase the macroprudential policy space in a stress situation. Such rebalancing could be implemented by introducing a positive rate for the CCyB under normal economic conditions, coupled with a thorough investigation of how such a change can best be achieved. Looking into the design and effectiveness of the macroprudential framework in place will be part of the evaluation and lessons learned agenda following the COVID-19 crisis.

The remaining articles in this issue of the Macroprudential Bulletin present the rationale and thinking behind selected policy choices and provide initial evidence on impediments related to market pressure and stigma.

References

Acharya, V., Le, H. and Shin, H.S. (2017), “Bank capital and dividend externalities”, The Review of Financial Studies, Vol. 30(3), March, pp. 988-1018.

Andreeva, D., Bochmann, P., and Couaillier, C. (2020), “Financial market pressure as an impediment to the usability of regulatory capital buffers”, European Central Bank, Macroprudential Bulletin, Issue 11, October.

BCBS (2011), “Basel III: A global regulatory framework for more resilient banks and banking systems – revised version”, Bank for International Settlements, June.

Borsuk, M., Budnik, K., and Volk, M. (2020), “Buffer use and lending impact”, European Central Bank, Macroprudential Bulletin, Issue 11, October.

- With comments from Karen Braun-Munzinger, Pascal Busch, Carsten Detken, Stephan Fahr, Matilda Gjirja, Marco Lo Duca, Enzo Mangone, Samuel McPhilemy, Fatima Pires, Evangelia Rentzou, Anton van der Kraaij, Thomas Voswinckel, Michael Wedow, Esther Wehmeier, and Balázs Zsámboki.

- See, for example, Acharya et al. (2017).

- For banks using the internal ratings-based approach, this would be due to increasing estimations of probability of default, loss given default and exposure at default, while for banks using the standardised approach, this would be due to downgrades by credit rating agencies and other risk identification/mitigation factors. For example, the crisis may have an adverse impact on collateral values, which increases loan-to-value (LTV) ratios for mortgages and may thus contribute to an increase in risk weights in the residential real estate portfolio (as mortgage loans with an LTV above 80% are subject to higher risk weight requirements).

- The active use of buffers operates via the increase in risk-weighted assets, as banks are not allowed to actively use buffers by reducing their regulatory capital (e.g. by distributing profits) to a level where they no longer meet the CBR (see Article 141(1) of the Capital Requirements Directive).

- The automatic distribution restrictions following a breach of the CBR imply a relative shift in investor returns from equity to bond holders. It is assumed that this relative shift is weaker in its effect than the signalling effect of the downgrade linked to the higher default risk.

- See the ECB press release “ECB supports macroprudential policy actions taken in response to coronavirus outbreak” of 15 April 2020. Through mandatory reciprocity, euro area banks further benefit from the CCyB reductions in the Czech Republic, Denmark, Hong Kong, Iceland, Norway, Sweden and the United Kingdom. See also the ECB communication “Macroprudential measures taken by national authorities since the outbreak of the coronavirus pandemic”.

- See the ECB press release “ECB Banking Supervision provides temporary capital and operational relief in reaction to coronavirus” of 12 March 2020.

- See, for example, “ECB Banking Supervision provides temporary capital and operational relief in reaction to coronavirus”, op. cit., “Basel Committee meets; discusses impact of Covid-19; reiterates guidance on buffers”, Bank for International Settlements, 17 June 2020, or “FSB Chair’s letter to G20 Finance Ministers and Central Bank Governors: July 2020”, FSB, July 2020.

- See the ECB press release “ECB extends recommendation not to pay dividends until January 2021 and clarifies timeline to restore buffers” of 28 July 2020.

- See “Introductory statement by Andrea Enria, Chair of the Supervisory Board of the ECB, at the virtual meeting of the European CFO Network organised by UniCredit Group”, ECB, 12 June 2020.