Euro area bank deposit costs in a rising interest rate environment

Published as part of the Financial Stability Review, May 2023.

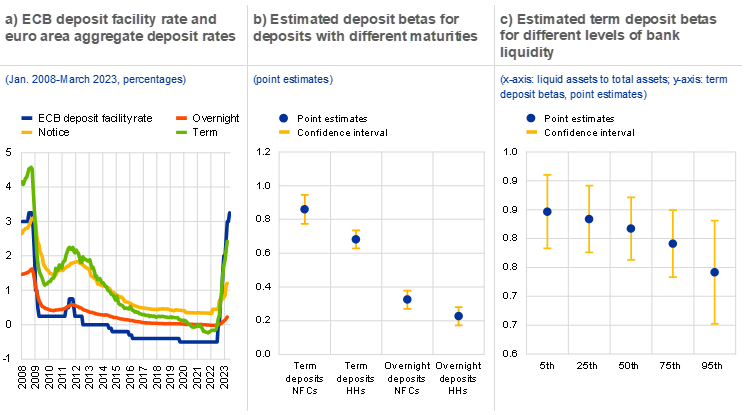

Changes in the cost and the composition of bank deposits have important implications for banks’ net interest income. This, in turn, affects their retained earnings, capital position, overall resilience and hence their ability to provide credit to the real economy. The ultimate impact of higher policy rates (Chart A, panel a) on banks’ net interest income depends, in particular, on the structure of their balance sheets and the sensitivity of their deposit and lending rates to policy rates.[1]

Chart A

Term deposit rates exhibit greater sensitivity than overnight deposit rates to policy rates, with some bank-specific characteristics also playing a role

Sources: ECB and ECB calculations.

Notes: Panel a: deposit rates refer to new business volumes and are calculated as the weighted average for non-financial corporations and households. Panel b: regressions are estimated through OLS panel fixed effect models based on a sample of 83 euro area banks and yearly data over the period from 2007 to 2021. The endogenous variables are the overnight and term deposit rates on new business from households and non-financial corporations. The variable of interest is the policy rate. Control variables include the lag of the endogenous variable, the logarithm of total assets, the return on assets, the ratio of deposits to total assets, the non-performing loans ratio, the liquid-assets-to-total assets ratio, the equity-to-total-assets ratio, the cost/income ratio, the change in the spread between the ten-year government bond yield and the German ten-year sovereign yield, GDP growth and the Herfindahl-Hirschman index. Control variables are all lagged by one period. Robust standard errors are clustered at the bank level. Confidence interval are at the 95% level. Panel c: the sample, the control variables and the fixed effects are the same as in panel b. The endogenous variable is the weighted average of new business term deposit rates for both non-financial corporations and households. The main variable of interest is the interaction between the policy rate and the ratio of liquid assets to total assets. The 5th, 25th, 50th, 75th and 95th percentiles correspond to a ratio of liquid assets equal to 3%, 8%, 15%, 27% and 48% respectively. Confidence intervals are at the 95% level.

Interest rates on “new” term deposits[2] for both non-financial corporations and households have risen since the start of the monetary policy tightening cycle, while overnight deposit rates have remained relatively sticky. Euro area banks have, to some extent, passed on increases in policy rates to the benefit of both non-financial corporations and households. This applies in particular to interest rates on term and notice deposits. Between June 2022 and March 2023, interest rates on term deposits increased by about 2.44 percentage points, interest rates on notice deposits increased by about 75 basis points respectively, while interest rates on overnight deposits increased only modestly, by about 25 basis points. In this context, the sensitivity of banks’ deposit rates to changes in interest rates, the so-called “deposit beta”, plays a key role.

The sensitivity of banks’ deposit rates to changes in policy rates depends on the type of deposit, bank-specific characteristics and the structure of the banking sector. Econometric analyses over the period 2007-21[3] reveal that about 86% (68%) of the change in policy rates is transmitted to rates on new term deposits from non-financial corporations (households), while 32% (23%) is transmitted to rates on overnight deposits from non-financial corporations (households) (Chart A, panel b).[4] Interest rates on new term deposits from non-financial corporations exhibit the highest sensitivity to changes in policy rates, as firms are more likely to switch to alternative investments and, until recently, were also charged negative deposit rates. The results also show that the pass-through of policy rates is lower in the case of larger and more liquid banks. For instance, a 1 percentage point increase in rates leads to a term deposit rate that is 12 basis points lower for larger banks and 10 basis points higher for less liquid banks (Chart A, panel c).[5] These sensitivities apply to new business and translate into a higher overall funding cost more slowly, in particular for term deposits which are only repriced on maturity.

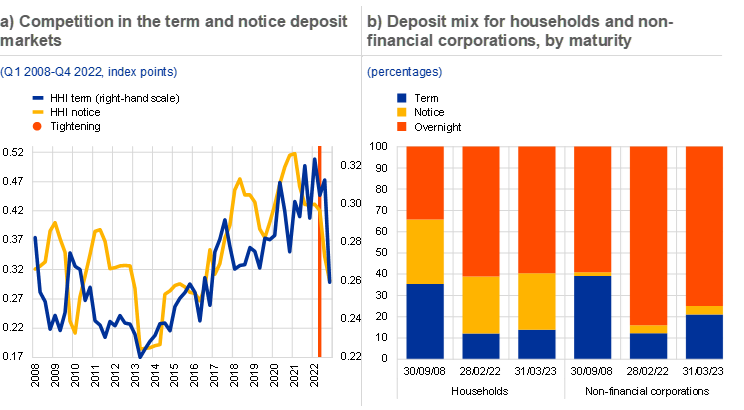

Deposit outflows and TLTRO repayments could intensify competition in the deposit market, leading to faster and higher deposit repricing than observed recently. In the four months following the first monetary policy tightening in the euro area, the Herfindahl-Hirschman index on term deposits and on notice deposits fell visibly (Chart B, panel a), indicating a sharp increase in competition for such deposits among euro area banks. Greater competition has already been reflected in higher rates for these deposits, especially for banks operating in more competitive markets, with negative implications for bank funding costs going forward.

Higher interest rates have increased non-financial corporations’ appetite for better remunerated deposit types, shifting banks’ deposit mix away from stickier overnight deposits towards rate-sensitive term deposits. The share of term deposits from non-financial corporations increased by about 9 percentage points between February 2022 and March 2023, while the share of overnight deposits from non-financial corporations declined to a similar extent (Chart B, panel b). Changes have so far been more limited for households, which also account for the majority of banks’ deposits. However, data prior to the low-for-long interest rate environment suggest that the share of term and notice deposits may increase further for both non-financial corporations and households, potentially weighing on total bank deposit funding costs going forward.

Chart B

Rising competition in the deposit market may lead to higher deposit betas, further exacerbated by a shift from stickier overnight deposits to rate-sensitive term deposits

Source: ECB and ECB calculations.

Notes: Panel a: the Herfindahl-Hirschman index (HHI) is calculated by squaring the market shares of the term or notice deposits of each bank operating in a country and then aggregating the resulting numbers. A lower HHI indicates stronger competition. Based on a sample of 158 euro area banks. Panel b: outstanding deposit volumes by maturity bucket and reported as a share of total deposits.

So far euro area banks have managed to contain the increase in deposit costs as the repricing of deposit rates has been limited, allowing them to benefit from higher net interest income. Rising competition and a reallocation of funds from overnight to term deposits might lead to an increase in funding costs that is faster and larger than expected. This could potentially translate into lower profitability for banks, impairing their ability to withstand adverse shocks – and hence their stability – at a time when the provision of credit is being inhibited by a less favourable macroeconomic environment and tighter financing conditions overall.

This box focuses mainly on deposits from households and non-financial corporations, which account for around 71% of the total deposits and 54% of the total liabilities of euro area banks (source ECB MFI Interest Rate Statistics).

Term deposits are deposits with an agreed maturity.

Findings are based on OLS panel fixed effects estimations. Specifically, deposit rates with different maturities are regressed on the policy rate as well as on bank- and country-specific characteristics, as defined in the notes to Chart A. One caveat to this analysis is the fact that the sample period under consideration includes mainly monetary easing episodes. This means that the results may not be a perfect guide to the behaviour of deposit rates going forward.

The point estimates for deposit betas are in line with the literature. See, for instance, De Graeve, F., De Jonghe, O. and Vander Vennet, R., “Competition, transmission, and bank pricing policies: Evidence from Belgian loan and deposit markets”, Journal of Banking & Finance, Vol. 31, Issue 1, 2007, pp. 259-278; Gropp, R., Kok, C. and Lichtenberger, J.D., “The dynamics of bank spreads and financial structure”, The Quarterly Journal of Finance, Vol. 4, No 4, 2014.

Larger (more liquid) banks are those banks at or above the 95th percentile of the total assets (liquid assets to total assets) distribution and are compared with smaller (less liquid) banks, which are those at or below the 5th percentile of the total assets (liquid assets to total assets) distribution.